BlackBerry (BB) shares ripped higher on April 20 after the embedded software firm announced an expanded partnership with the artificial intelligence (AI) sector leader Nvidia (NVDA).

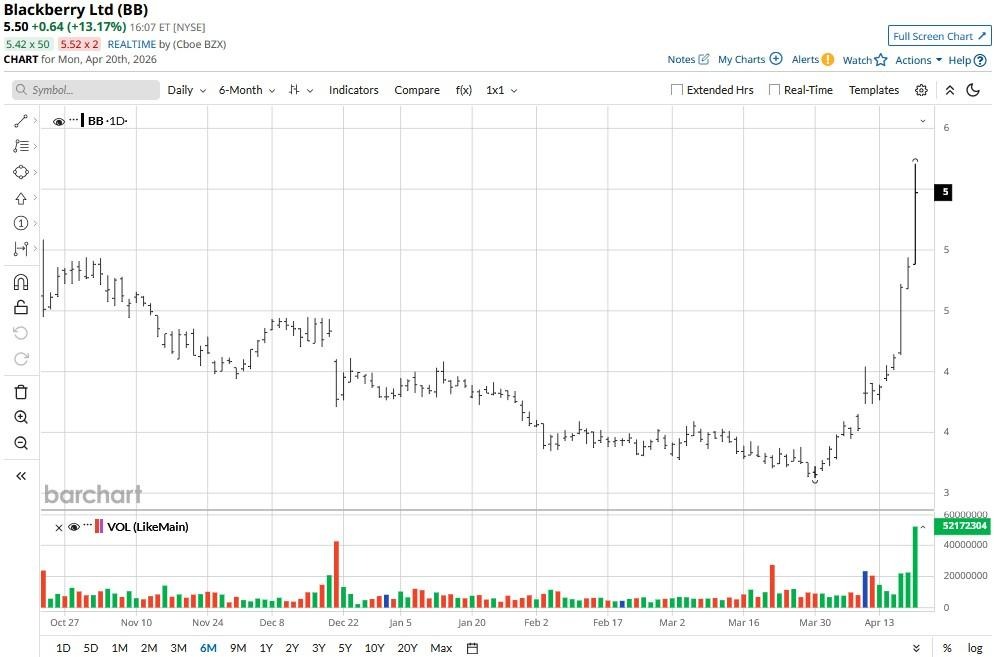

The upward momentum pushed BB’s relative strength index (14-day) into the early 90s, signaling the Canadian company may be due for a near-term pullback.

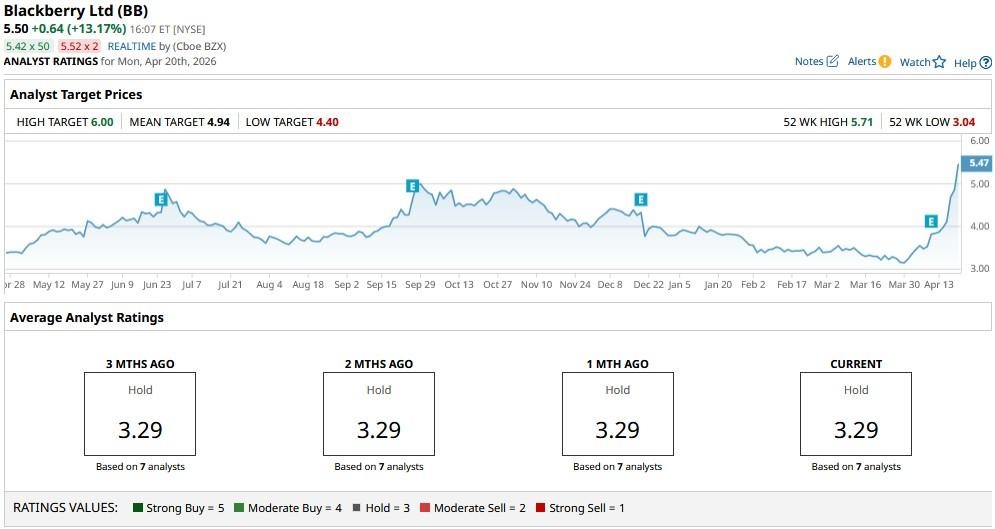

BlackBerry stock has been an exciting investment for investors in April, currently up an incredible 75% versus the start of this month.

Significance of the NVDA Deal for BlackBerry Stock

BlackBerry is expanding the integration of its QNX OS for Safety 8.0 into the NVDA IGX Thor platform.

While the two companies have a long history in the automotive space, this deal specifically targets the burgeoning “Edge AI” market, spanning medical robotics, industrial automation, and smart manufacturing.

It’s bullish for BB shares because it cements QNX as the essential safety-and-control layer for the world’s most advanced AI hardware.

By becoming the “brain” that ensures Nvidia's high-speed artificial intelligence processing remains safe and predictable in regulated environments, BlackBerry is effectively diversifying its revenue beyond cars.

For investors, this partnership validates its pivot from a legacy handset maker to a high-margin, indispensable software backbone for the AI-driven industrial revolution.

Why BB Shares Still Aren’t Worth Owning

Despite this team-up with the AI darling, investors are advised to exercise caution in buying BlackBerry shares at current levels, mostly because of valuation concerns.

At about 36x forward earnings, BB isn’t more expensive than its software peers; it actually dwarfs NVDA's multiple (just 25x currently).

This makes BlackBerry less attractive, especially since its legacy cybersecurity business remains a drag on its overall performance as well.

Recent reports suggest a dollar-based net retention rate (DBNRR) of 94%. Anything below 100% signals a business is losing more revenue from existing clients than it’s gaining through expansions.

Plus, the pivot to physical AI, while visionary, means longer sales cycles than consumer software, making it even more difficult to justify sticking with BB in 2026.

How Wall Street Recommends Playing BlackBerry

Wall Street’s current estimates for BlackBerry also warrant trimming exposure to it at the current price.

The consensus rating on BB stock sits at a “Hold," with the mean price target of $4.94 indicating potential downside of about 10% from here.