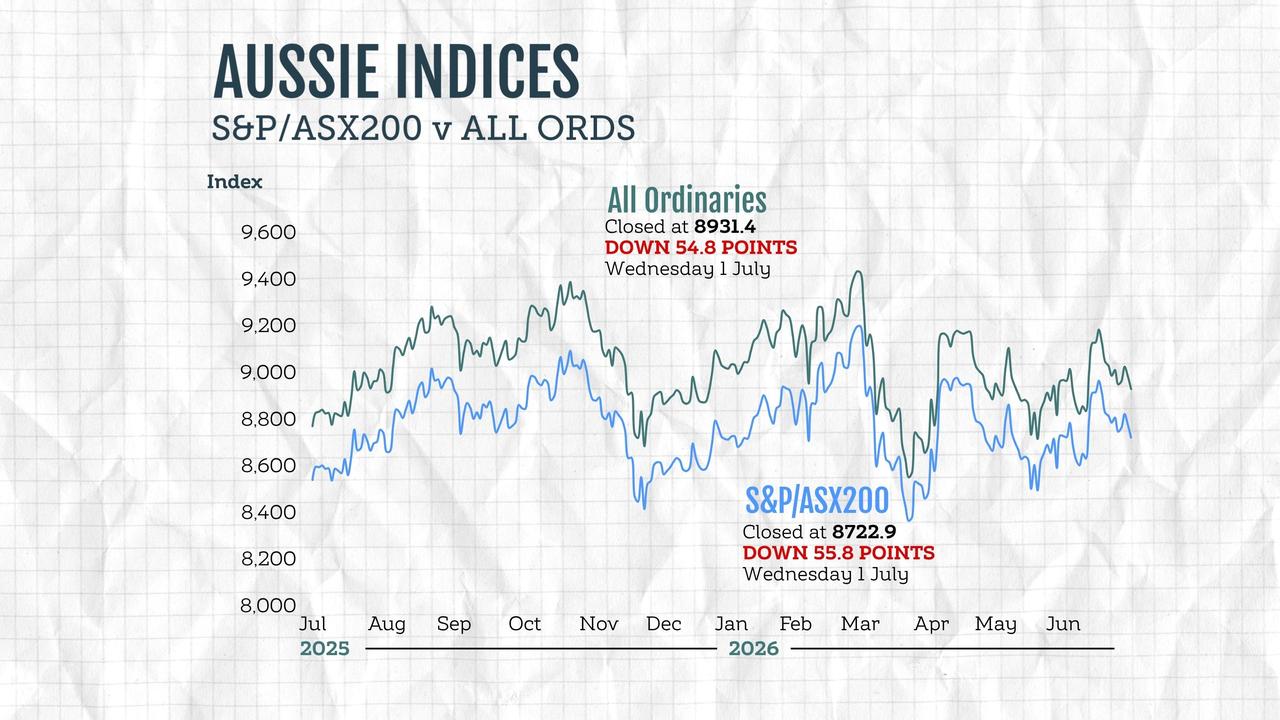

Australia's share market has had a dour start to the new financial year, dropping for the seventh time out of its past 10 sessions after a sell-off in banking and supermarket stocks.

The benchmark S&P/ASX200 index on Wednesday finished 55.8 points lower at 8,722.9, a drop of 0.64 per cent, while the broader All Ordinaries fell 54.8 points, or 0.61 per cent, to 8,931.4.

The ASX200 ended the day at its lowest level in 20 days and up less than 0.1 per cent since the start of 2026.

All the major banks fell sharply, pulling the financial sector down 1.7 per cent.

ANZ lost 2.5 per cent to $34.47 in its worst daily performance since May 1, while the other three big retail banks were close behind.

CBA fell 2.4 per cent to $160.73, NAB retreated 2.3 per cent to $36.99 and Westpac subtracted 1.5 per cent to $34.70.

In the consumer staples sector, Coles suffered its worst drop since the war with Iran began on February 27, falling 4.2 per cent to $23.35 as the supermarket giant said it was considering the potential purchase of Petbarn owner Greencross from private equity firm TPG.

The drop likely shows investors were worried the potential acquisition would be a distraction from chief executive chief executive Leah Weckert's successful simplification strategy, analysts said.

Woolworths fell 1.8 per cent to $39.31 while the consumer staples sector as a whole dropped 2.1 per cent.

A total of seven of the ASX's 11 sectors were lower, while energy, materials, health care and utilities finished higher.

The sector split was a fitting reminder of the key lesson from the financial year that just finished, said Betashares investment strategist Tom Wickenden.

That lesson was Australian equities remained highly dependent on narrow pockets of leadership while investors searched for the next source of broad earnings growth, he said.

The biggest loser in the ASX300 was Objective Corp, which crashed 34.5 per cent to a six-year low of $6.75 after the public sector software company lost a longstanding software contract on short notice.

Objective Corp chief executive Tony Walls said the company he founded was "deeply disappointed" with the Australian defence department's decision, which came after months of negotiations.

On the flip side, Perpetual rose 15.5 per cent to a six-month high of $17.90 before the wealth manager's shares were placed in a trading halt pending an announcement about a potential takeover offer.

In the heavyweight mining sector, South32 rose 9.7 per cent to a two-week high of $4.28 after the company said it would sell its aluminium businesses to Alcoa for up to $US5.6 billion ($8 billion).

The assets include South32's majority stake in the bauxite mining and alumina refining operation in Western Australia known as Worsley Alumina, as well as operations in South Africa and Brazil.

The transaction will reposition South32 as a base metals company focused on copper, zinc, silver and lead.

Elsewhere in the sector, BHP rose 0.9 per cent to $59.92, Fortescue climbed 0.5 per cent to $19.24 and Rio Tinto dropped 1.0 per cent to $170.81.

The Australian dollar was trading for 68.90 US cents, from 68.77 US cents at 5pm on Tuesday.

ON THE ASX:

* The S&P/ASX200 on Wednesday fell 55.8 points, or 0.64 per cent, to 8,722.9

* The broader All Ordinaries lost 54.8 points, or 0.61 per cent, to 8,931,4

One Australian dollar trades for:

* 68.90 US cents, from 68.77 US cents at 5pm AEST on Tuesday

* 112.10 Japanese yen, from 111.55 Japanese yen

* 60.43 euro cents, from 60.30 euro cents

* 52.04 British pence, from 51.92 pence

* 121.46 NZ cents, from 121.60 NZ cents