/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

Broadcom (AVGO) stock tumbled on Thursday even though the semiconductor behemoth reported better-than-expected earnings for its second quarter.

Investors are responding primarily to a slight miss on revenue that printed at $22.19 billion.

Moreover, management didn’t present a new catalyst or reveal a fresh marquee AI customer, which further disappointed a demanding market that had been expecting blowout numbers and exciting announcements from AVGO.

Despite the post-earnings pullback, however, Broadcom stock remains a solid investment for 2026, still up a remarkable 40% versus its year-to-date low.

Why Chip Stocks Sold Off After Broadcom Earnings

Broadcom is a structural bellwether for the semiconductor sector; its mixed commentary, therefore, sent shockwaves through the entire chip complex.

On the earnings call, the Nasdaq-listed firm didn’t raise its AI semiconductor sales forecast (2026), making investors question its stretched forward price-to-earnings (P/E) multiple of roughly 48x.

In Q2, AVGO’s artificial intelligence chip sales increased 143% on a year-over-year basis to $10.8 billion.

But the mix heavily favored custom application-specific integrated circuits (ASICs) over standard silicon, and since ASICs aren’t as profitable as generic hardware, management hinted at near-term pressure on margins, which spooked investors.

This margin anxiety quickly translated into sector-wide selling, dragging the likes of Nvidia (NVDA), AMD (AMD), Micron (MU), Arm (ARM), Marvell (MRVL), and others down with it, as investors feared that the hyper-profitable phase of the AI infrastructure buildout is now normalizing.

Should You Buy the Dip in AVGO Shares Today?

For long-term investors, the post-earnings weakness in Broadcom shares is an opportunity to buy, says Jefferies’ senior analyst Blayne Curtis.

In a research note dated June 4, Curtis raised his price target on AVGO to $550, indicating potential upside of a whopping 31% from current levels.

According to him, while ASIC mix-shifts pressure metrics in the near-term, operating margins are positioned to expand dramatically as custom silicon programs for major hyperscalers — specifically Meta (META) and OpenAI — begin to ramp heavily next year.

Broadcom’s secular dominance in AI networking and a 0.62% dividend yield make today’s dip worth buying, the Jefferies analyst concluded.

How Wall Street Recommends Playing Broadcom

While not as bullish as Jefferies, other Wall Street firms haven’t thrown in the towel on Broadcom either.

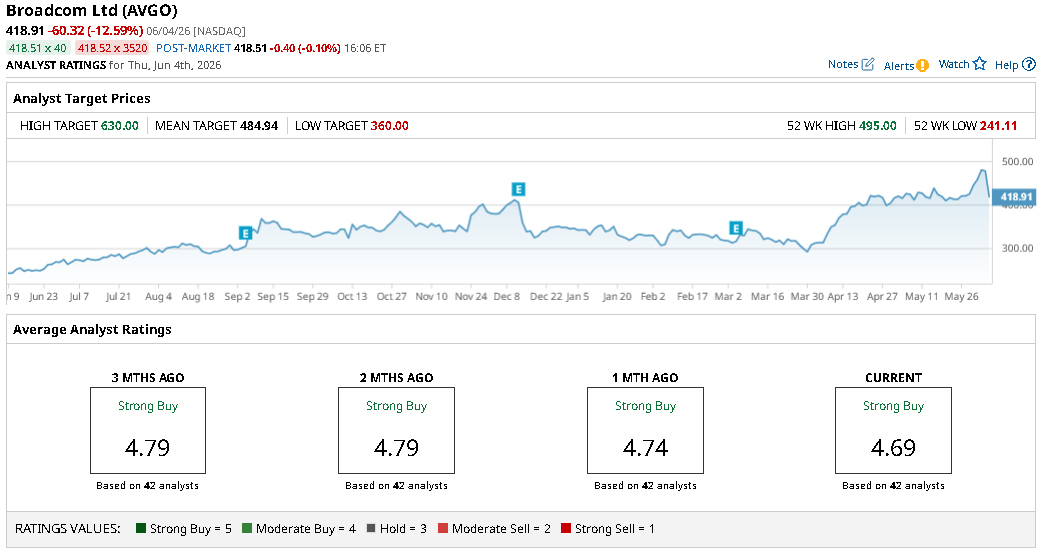

The consensus rating on AVGO shares sits at “Strong Buy,” with the mean price objective of nearly $485, indicating potential for a 15% rally from here.