Throughout the last three months, 11 analysts have evaluated Williams Companies (NYSE:WMB), offering a diverse set of opinions from bullish to bearish.

In the table below, you'll find a summary of their recent ratings, revealing the shifting sentiments over the past 30 days and comparing them to the previous months.

| Bullish | Somewhat Bullish | Indifferent | Somewhat Bearish | Bearish | |

|---|---|---|---|---|---|

| Total Ratings | 4 | 3 | 4 | 0 | 0 |

| Last 30D | 0 | 0 | 1 | 0 | 0 |

| 1M Ago | 1 | 1 | 1 | 0 | 0 |

| 2M Ago | 2 | 2 | 2 | 0 | 0 |

| 3M Ago | 1 | 0 | 0 | 0 | 0 |

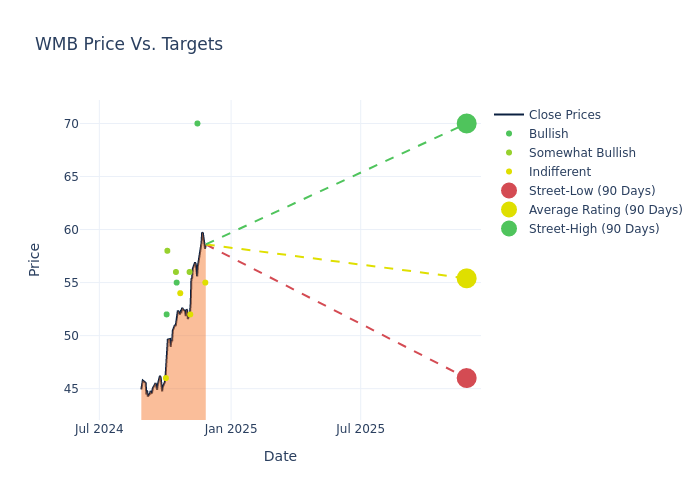

Analysts' evaluations of 12-month price targets offer additional insights, showcasing an average target of $55.36, with a high estimate of $70.00 and a low estimate of $46.00. Observing a 17.54% increase, the current average has risen from the previous average price target of $47.10.

Exploring Analyst Ratings: An In-Depth Overview

The standing of Williams Companies among financial experts becomes clear with a thorough analysis of recent analyst actions. The summary below outlines key analysts, their recent evaluations, and adjustments to ratings and price targets.

| Analyst | Analyst Firm | Action Taken | Rating | Current Price Target | Prior Price Target |

|---|---|---|---|---|---|

| John Mackay | Goldman Sachs | Raises | Neutral | $55.00 | $45.00 |

| Shneur Gershuni | UBS | Raises | Buy | $70.00 | $55.00 |

| Neal Dingmann | Truist Securities | Raises | Hold | $52.00 | $42.00 |

| Gabriel Moreen | Mizuho | Raises | Outperform | $56.00 | $47.00 |

| Robert Catellier | CIBC | Raises | Neutral | $54.00 | $45.00 |

| Jean Ann Salisbury | B of A Securities | Announces | Buy | $55.00 | - |

| Elvira Scotto | RBC Capital | Raises | Outperform | $56.00 | $47.00 |

| Robert Kad | Morgan Stanley | Raises | Overweight | $58.00 | $52.00 |

| Spiro Dounis | Citigroup | Raises | Buy | $52.00 | $45.00 |

| Theresa Chen | Barclays | Raises | Equal-Weight | $46.00 | $42.00 |

| Shneur Gershuni | UBS | Raises | Buy | $55.00 | $51.00 |

Key Insights:

- Action Taken: Analysts adapt their recommendations to changing market conditions and company performance. Whether they 'Maintain', 'Raise' or 'Lower' their stance, it reflects their response to recent developments related to Williams Companies. This information provides a snapshot of how analysts perceive the current state of the company.

- Rating: Unveiling insights, analysts deliver qualitative insights into stock performance, from 'Outperform' to 'Underperform'. These ratings convey expectations for the relative performance of Williams Companies compared to the broader market.

- Price Targets: Analysts set price targets as an estimate of a stock's future value. Comparing the current and prior price targets provides insight into how analysts' expectations have changed over time. This information can be valuable for investors seeking to understand consensus views on the stock's potential future performance.

Analyzing these analyst evaluations alongside relevant financial metrics can provide a comprehensive view of Williams Companies's market position. Stay informed and make data-driven decisions with the assistance of our Ratings Table.

Stay up to date on Williams Companies analyst ratings.

About Williams Companies

Williams Companies is a midstream energy company that owns and operates the large Transco and Northwest pipeline systems and associated natural gas gathering, processing, and storage assets. In August 2018, the firm acquired the remaining 26% ownership of its limited partner, Williams Partners.

Financial Insights: Williams Companies

Market Capitalization Highlights: Above the industry average, the company's market capitalization signifies a significant scale, indicating strong confidence and market prominence.

Revenue Growth: Williams Companies's remarkable performance in 3 months is evident. As of 30 September, 2024, the company achieved an impressive revenue growth rate of 3.67%. This signifies a substantial increase in the company's top-line earnings. When compared to others in the Energy sector, the company faces challenges, achieving a growth rate lower than the average among peers.

Net Margin: The company's net margin is a standout performer, exceeding industry averages. With an impressive net margin of 26.57%, the company showcases strong profitability and effective cost control.

Return on Equity (ROE): Williams Companies's ROE falls below industry averages, indicating challenges in efficiently using equity capital. With an ROE of 5.72%, the company may face hurdles in generating optimal returns for shareholders.

Return on Assets (ROA): Williams Companies's ROA is below industry averages, indicating potential challenges in efficiently utilizing assets. With an ROA of 1.33%, the company may face hurdles in achieving optimal financial returns.

Debt Management: Williams Companies's debt-to-equity ratio is below the industry average. With a ratio of 2.19, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

The Significance of Analyst Ratings Explained

Benzinga tracks 150 analyst firms and reports on their stock expectations. Analysts typically arrive at their conclusions by predicting how much money a company will make in the future, usually the upcoming five years, and how risky or predictable that company's revenue streams are.

Analysts attend company conference calls and meetings, research company financial statements, and communicate with insiders to publish their ratings on stocks. Analysts typically rate each stock once per quarter or whenever the company has a major update.

Analysts may supplement their ratings with predictions for metrics like growth estimates, earnings, and revenue, offering investors a more comprehensive outlook. However, investors should be mindful that analysts, like any human, can have subjective perspectives influencing their forecasts.

Breaking: Wall Street's Next Big Mover

Benzinga's #1 analyst just identified a stock poised for explosive growth. This under-the-radar company could surge 200%+ as major market shifts unfold. Click here for urgent details.

This article was generated by Benzinga's automated content engine and reviewed by an editor.