/United%20Parcel%20Service%2C%20Inc_%20logo%20magnified-by%20Casimiro%20PT%20via%20Shutterstock.jpg)

United Parcel Service (UPS) recorded a slump in both profit and revenue for its fiscal first quarter on Tuesday, but promised inflection ahead as it continues to move away from Amazon (AMZN) deliveries.

In Q1, Amazon represented less than 9% of the total UPS revenue, down from north of 13% not long ago, with an additional 500,000 average daily packages removed during the quarter.

On Tuesday, UPS slipped through its 50-day and 100-day moving averages (MAs), indicating that bearish momentum could continue in the near term.

Versus its year-to-date high, United Parcel Service stock is now down about 13%.

What Shifting Away From Amazon Means for UPS Stock

Moving away from Amazon is bullish for UPS shares because the e-commerce giant’s low-margin, high-volume shipments tend to drag on profitability.

As AMZN builds its own logistics network, United Parcel Service has been intentionally shifting its mix toward SMBs, healthcare, and high-value commercial clients that generate stronger yields per package.

Small and medium businesses accounted for a record 34.5% of total U.S. volume in Q1, and healthcare revenue hit a milestone $3 billion quarterly run rate.

Reducing Amazon exposure improves pricing power, as evidenced by a 6.5% increase in revenue per piece domestically and an even higher 10.7% increase internationally.

Why Else Are United Parcel Service Shares Attractive?

Long-term investors should consider buying the dip in United Parcel Service shares because CEO Carol Tomé framed Q1 as the trough, adding that the critical transition period is now in the rearview mirror.

UPS expects to return to consolidated revenue and operating profit growth in the current quarter, with U.S. domestic margins projected to hit as much as 8.5%.

Moreover, the company remains on track for a $3 billion cost-savings target for 2026, supported by nearly 25,000 operational position reductions year-over-year and continued automation investments.

An attractive price-to-sales (P/S) ratio of 1.02x and a rather lucrative 6.33% dividend yield make up for additional reasons to stick with United Parcel Service.

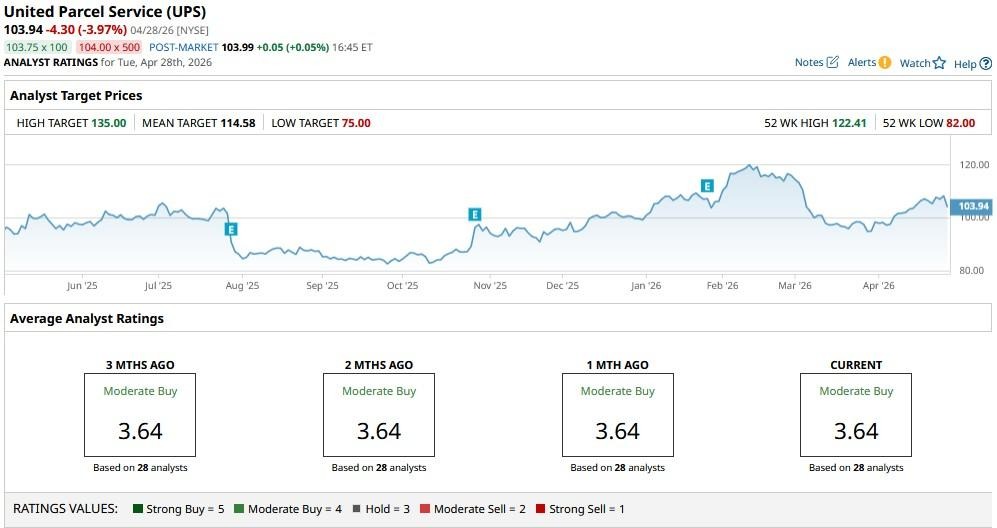

What’s the Consensus Rating on United Parcel Service?

Wall Street also remains bullish on UPS stock, especially because, despite a year-over-year decline, the company came in ahead of Q1 estimates and reaffirmed its full-year guidance.

The consensus rating on United Parcel Service sits at “Moderate Buy,” with the mean price target of just over $114 indicating potential upside of roughly 10% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.