/Facebook%20like%20button%20on%20keyboard%20by%20athree23%20via%20Pixabay.jpg)

The broader markets are looking weak as the war in Iran continues to escalate, pushing up oil prices. To make things worse, U.S. wholesale inflation rose more than expected in February. While inflation being stubbornly above the Fed’s 2% target wasn’t really a secret, Fed Chair Jerome Powell summed up the state of U.S. inflation at his post-meeting press conference and said, “The forecast is that we will be making progress on inflation, not as much as we had hoped, but some progress on inflation.”

Meanwhile, even though the S&P 500 Index ($SPX) has fallen over 5% from its record highs, there has been a brutal selloff in some pockets, particularly tech and software stocks. Specifically, Meta Platforms (META) has fallen 18% from its 2026 highs and is trading near its lows for the year, falling towards the $600 price levels. Let's dig into whether it's time to buy the dip in META stock or if investors would be better off staying on the sidelines.

Meta Stock Forecast

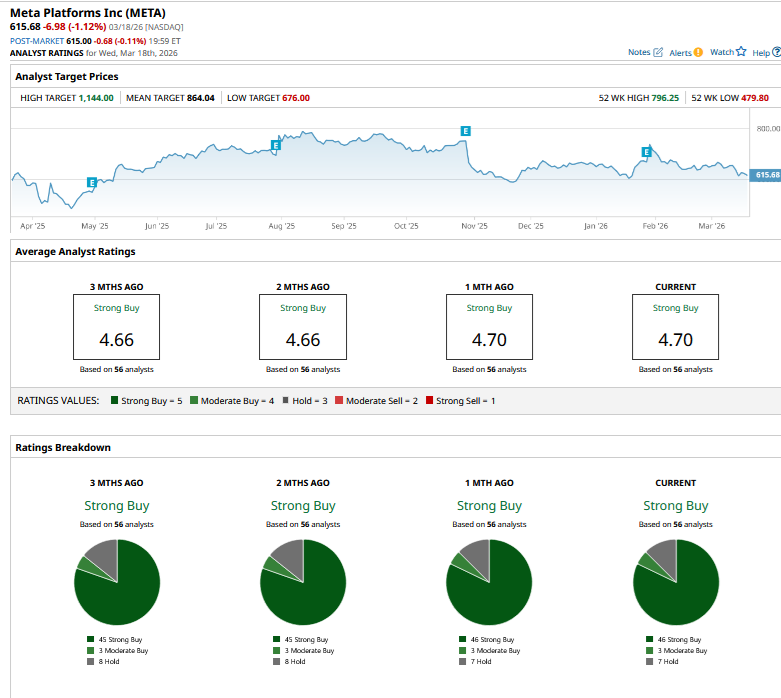

Despite the dip, brokerages are quite upbeat on META stock, and it has a consensus rating of “Strong Buy” from the 56 analysts polled by Barchart. The stock’s mean target price is $864.04, which is 42% higher than the current price levels. Here, it is worth noting that sell-side analysts haven’t tweaked their target prices for Meta—or, for that matter, many other stocks—amid the Iran war. However, the conflict has continued for much longer than some expected, and there looks to be no off-ramp for now.

Key Risks Meta Investors Should Watch Out For

If the situation does not improve and crude oil continues to hover around $100 per barrel, it would negatively impact global growth. The repercussions would also be felt on global ad spend, which is the bread and butter for Meta. There is also the direct cost of higher energy prices, as running costs for Meta’s data centers would also rise.

Another factor that investors should be watching is the growing clamor for banning or restricting social media for children. Australia has already banned kids below 16 from using social media, becoming the first country to do so. Several European countries are at various stages of enforcing a ban on social media for kids. In Asia, Indonesia and Malaysia plan to ban social media for children. In India, which is the biggest market for Meta in terms of users, the state of Karnataka has banned children below 16 from using social media, while some other states are contemplating such policies.

While enforcing these bans won't be an easy task, “catching 'em early” has helped spur growth for social media companies like Meta Platforms, and losing out on teens would negatively impact their growth.

Meta Is Doubling Down on AI

Meanwhile, Meta is doubling down on artificial intelligence (AI) and expects its 2026 capex to be between $115 billion and $135 billion, which is significantly higher than last year's capex of $72.2 billion. Notably, while markets have been wary of tech companies’ burgeoning capex, Meta actually soared after the Q4 2025 earnings release despite announcing the massive rise in AI capex. The price action could be attributed to the strong revenue growth that Meta is delivering, unlike many of its Big Tech peers, for whom AI capex growth is not leading to adequate topline growth.

Meta has also been quite aggressive with cost cuts, and more layoffs might be around the corner. The company also scaled back its metaverse bet and expects Reality Labs’ segment losses to peak in 2026. For context, the segment posted an operating loss of over $6 billion in Q4, while cumulative losses since 2020 have topped $80 billion. The company’s profitability should improve in 2027 and beyond as Reality Labs losses (hopefully) narrow while overall expense growth moderates.

Should You Buy META Stock?

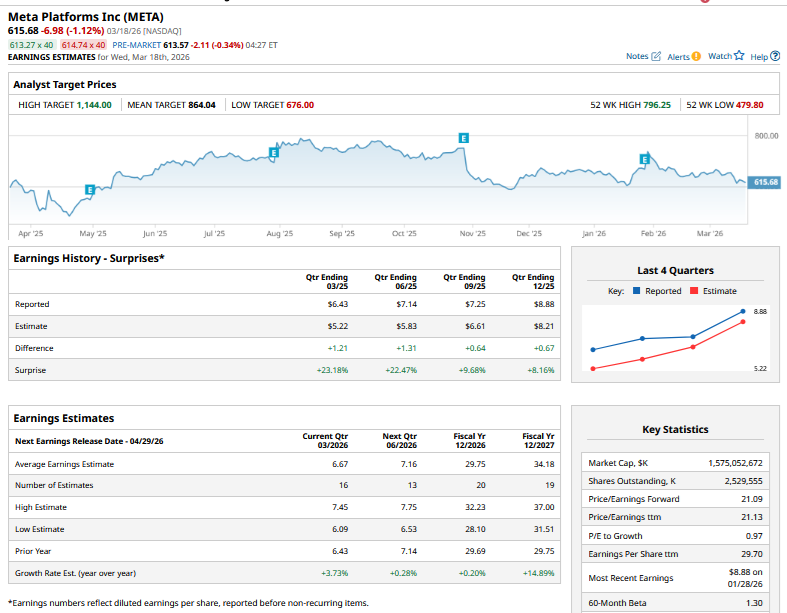

Meta’s valuation multiples have contracted after the crash, and it now trades at a forward price-to-earnings (P/E) multiple of just over 21x. The multiples are still higher than historical averages but below what we have seen over the last couple of years.

All said, while it is difficult to price in events like the Iran war, where both sides are not shying away from escalation, I find META stock attractive for long-term investors. However, investors should brace for short-term volatility as the geopolitical situation in the Middle East might continue to weigh heavily on markets.