/Alphabet%20Inc_%20and%20Google%20logos%20seen%20displayed%20on%20a%20smartphone%20by%20IgorGolovniov%20via%20Shutterstock.jpg)

With a year-to-date gain of 26%, Alphabet (GOOG) (GOOGL) is the best-performing Magnificent 7 stock. The Google parent was the best-performing constituent of the coveted group last year and has continued its good run in 2026 as well.

Meanwhile, thanks to the recent rally, the stock is now approaching $400 levels. Moreover, it is on the verge of becoming the next $5 trillion company. No other company apart from Nvidia (NVDA) has achieved that feat. Notably, artificial intelligence (AI) has redefined the market cap pecking order among Big Tech companies, and companies such as Meta Platforms (META) and Microsoft (MSFT), which have failed to justify their burgeoning capex, have fallen out of favor with investors.

Until about a few months back, Nvidia was the predominant AI play as its chips were the basic building block for the massive data centers that Big Tech companies are building. However, Alphabet has been the market’s latest AI darling as it is not only witnessing impressive monetization of its capex but is now looking to compete with Nvidia by offering its own chips to third-party customers.

Alphabet’s Cloud Backlog Doubled in Q1 2026

While Alphabet does not provide standalone numbers for its tensor processing unit (TPU) and graphics processing units (GPUs), during the Q1 2026 earnings call, it said that its chips are part of the $462 billion cloud backlog, which incidentally doubled in the quarter. Moreover, Alphabet’s cloud revenues rose 63% year-over-year in Q1, and the segment’s quarterly sales topped $20 billion for the first time. The company has been gaining cloud market share from Amazon Web Services (AWS) (AMZN) and Microsoft Azure, which grew at a much slower pace in Q1.

TPUs Could Be a Key Revenue Driver for Alphabet

Alphabet expects to “begin to deliver TPUs to a select group of customers in their own data centers.” It expects some revenues from these deals later this year, but the bulk of the revenues from the current deals will flow in 2027. Citizens JMP, which has a “Market Outperform” rating on GOOG, expects TPU sales to reach about $3 billion in 2026 while projecting them to rise to $25 billion in 2027.

While OpenAI’s woes have taken a toll on Microsoft shares, Alphabet is riding the Anthropic wave. The AI startup has impressed with its models, and thanks to its soaring valuations, Alphabet’s stake in the company is now over $50 billion. Separately, filings showed that Alphabet owns over a 6% stake in SpaceX, which could be valued north of $100 billion if the Elon Musk-run company goes public at the kind of valuations that are floating around.

GOOG Stock Forecast

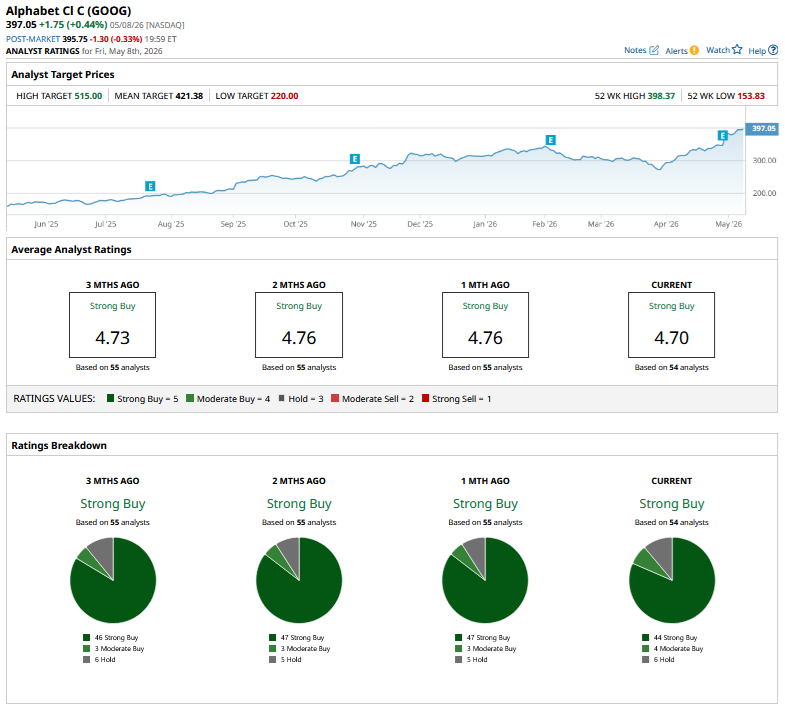

I did not expect a major rally in GOOG following the Q1 earnings, but the results were stellar, to say the least. The stock saw a nearly double-digit rise following the confessional, which is the highest among its Mag 7 peers, barring Nvidia, which is yet to report its earnings. After Alphabet’s Q1 earnings release, brokerages including TD Cowen, Scotiabank, and JPMorgan raised the stock’s target prices. GOOG has a mean target price of $421.38, which is just over 6% higher than current prices.

Should You Buy GOOG Stock?

Alphabet trades at a forward price-to-earnings (P/E) multiple of 28x, which is higher than its historical averages. However, I won't harp much on the “history” part here as markets are currently valuing Big Tech companies based on their progress in AI — either actual or perceived. To its credit, Alphabet has emerged as an AI winner, and the company has successfully allayed fears of it losing its turf in search to AI upstarts. Moreover, its cloud segment has been consistently growing at a much faster pace than its major competitors.

All said, while I remain bullish on Google, I don't see much heat left in the rally in the short term and won't be averse to booking profits at these levels. However, I would be watching for any downward pressure in GOOG amid the broader market weakness to add more shares.