/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

CoreWeave (CRWV) is a specialized cloud computing company delivering GPU-powered infrastructure tailored for AI workloads, machine learning, VFX rendering, and high-performance computing. It provides scalable access to Nvidia (NVDA) GPUs via Kubernetes clusters, auto-scaling storage, and developer-friendly tools, helping enterprises train massive models faster and cheaper than general clouds.

Founded in 2017 by ex-crypto miners, CoreWeave is headquartered in Livingston, New Jersey. The company has data centers primarily in the U.S. (28-plus sites) and is expanding intp Europe (the U.K., Norway, Sweden, Spain), supporting global clients.

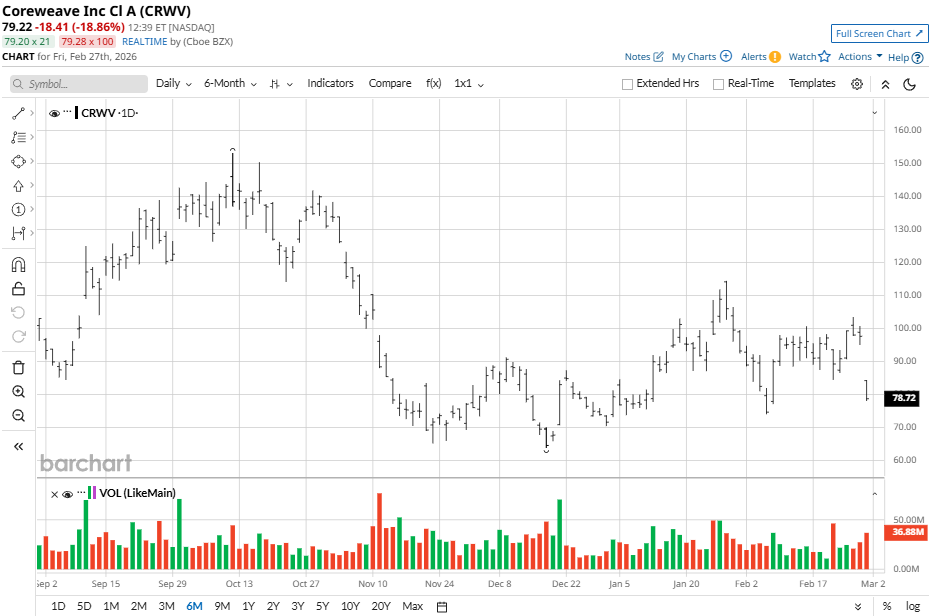

CoreWeave Stock Drops From Highs

Since its March 2025 initial public offering (IPO) at $40, CRWV stock has been highly volatile amid AI hype. Currently trading near $79, the stock is up sharply from its 52-week low of $33.51 but down 58% from the 52-week high of $187. Recent five-day action shows that the stock has slipped 21% while the past one-month period reveals a 6% drop. Mixed with the 50-day moving average (MA) at $88.16 versus the 200-day MA at $110.06, the 52-week range reflects massive swings, while year-to-date (YTD) the stock is up 8% despite being off its highs.

Coreweave stock underperforms compared to the Nasdaq Composite ($NASX), with the index showing a positive six-month report, gaining 4% against CRWV stock’s 12% fall. Still, AI catalysts keep CRWV punchier short-term versus index steadiness.

CoreWeave Reports Mixed Results

CoreWeave crushed revenue expectations in the fourth quarter of 2025 with $1.57 billion in sales — up 110% year-over-year (YOY) — fueled by surging AI GPU demand from hyperscalers like Microsoft (MSFT) and OpenAI. Full-year revenue came in at $5.1 billion, marking 168% YOY growth. However, EPS missed at a loss of $0.89 versus an estimated loss of $0.49, as net loss ballooned to $452 million amid aggressive expansion. Shares slipped post-earnings on conservative guidance.

Additional key metrics for the period include adjusted EBITDA of $898 million (slightly missing estimates of $929 million) with a 57% margin. Backlog exploded to $66.8 billion, while customer concentration eased. Operating expenses rose to $1.66 billion during Q4, while interest hit $388 million. Strong liquidity supports CoreWeave's capex ramp.

The company provided a cautious outlook to investors with projected Q1 revenue of $1.9 billion to $2 billion, coming in below the $2.29 billion estimate. For fiscal 2026, the company foresees $12 billion to $13 billion in revenue, adjusted operating income of $900 million to $1.1 billion, and capex of $30 billion to $35 billion (contract-backed). Margins trough early then expand to low double-digits by year-end, prioritizing capacity for the AI boom.

CoreWeave Is Looking to Fund the Meta Deal

CoreWeave is negotiating $8.5 billion in delayed-draw term loans from banks like Morgan Stanley (MS) and Mitsubishi UFJ Financial Group (MUFG) to fund massive cloud computing expansion for Meta Platforms (META). The loan leverages CoreWeave's $14.2 billion contract with Meta from last year, covering GPU-powered AI services, plus a newly revealed $5 billion-plus deal from early 2026, totaling over $19 billion in backing.

This structure lets CoreWeave draw funds incrementally as needed rather than upfront, with Meta's strong credit profile likely securing an investment-grade rating despite CoreWeave's junk status, slashing interest costs. Banks are quietly syndicating to others, targeting a March 2026 close.

The move fits CoreWeave's debt-heavy growth strategy amid the AI infrastructure frenzy. Existing debt hit $14 billion (including $8 billion in prior GPU loans) plus $2.25 billion convertibles. AI firms tapped $200 billion-plus in private debt last year, and 2026 could double that.

Should You Buy CRWV Stock?

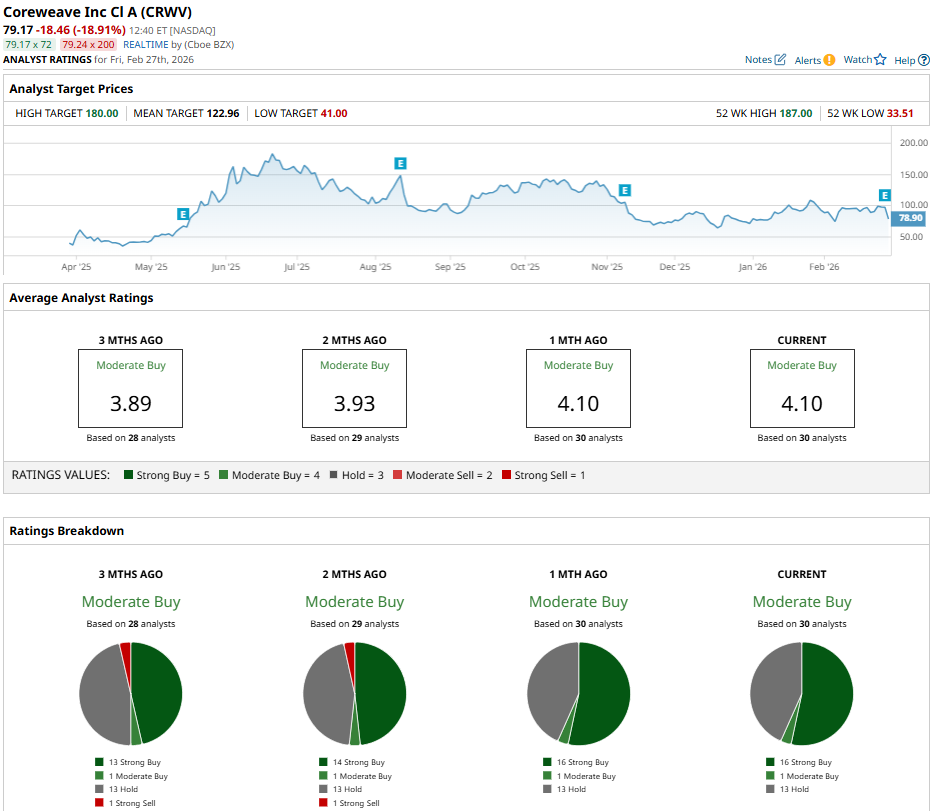

As CRWV stock continues to suffer from volatility, analysts offer a consensus “Moderate Buy” rating with a mean price target of $120.61, reflecting potential upside of 53% from current levels. The stock has been rated by a total of 30 analysts, with 16 “Strong Buy” ratings, one “Moderate Buy” rating, and 13 “Hold” ratings.