For years, billionaire investor Warren Buffett avoided airline stocks, calling the industry a capital trap – vulnerable to fuel spikes, fare wars, and economic shocks. When COVID-19 hit, Berkshire Hathaway (BRK.A) (BRK.B) dumped its airline holdings in 2020 at heavy losses, with Buffett admitting, “The world has changed for the airlines. And I don't know how it's changed and I hope it corrects itself in a reasonably prompt way .”

Hence, Wall Street is paying close attention now. After years of skepticism toward the sector, Berkshire has quietly returned to the sector with a massive $2.6 billion investment in Delta Air Lines (DAL), representing a sharp reversal that suggests Buffett sees something different this time around. And Delta’s Q1 2026 numbers offer some explanation.

The airline posted record revenue of $14.2 billion, marking a 9.4% annual growth, while Q1 adjusted EPS jumped 42%. Delta also generated $1.2 billion in FCF and delivered a solid 12% return on invested capital. The company has been cutting less-profitable routes, raising fares to offset higher fuel costs, and aggressively targeting higher-spending travelers. Corporate bookings hit record levels, premium cabin demand stayed strong across global routes, and its American Express (AXP) partnership generated $2 billion in quarterly revenue. Even with jet fuel prices surging alongside Middle East tensions, DAL stock has still climbed 52% over the past 52 weeks and is up 5.73% in 2026.

But while Buffett is buying into Delta’s resilience, billionaire hedge fund manager David Tepper is taking a very different approach. His firm, Appaloosa Management, disclosed in its latest 13F filing that it exited positions in American Airlines Group (AAL) and United Airlines Holdings (UAL) during Q1. This reflects growing concerns around rising jet fuel costs, tighter profit margins, softer travel demand risks, and mounting geopolitical uncertainty that could pressure the broader airline industry.

With one legendary investor buying into airlines again while another billionaire fund manager heads for the exit, let’s take a closer look at AAL and UAL, and what may come next.

Airline Stock #1: American Airlines

American Airlines Group is one of the world’s largest airline networks, connecting more than 350 destinations across over 60 countries through thousands of daily flights. Headquartered in Fort Worth, Texas, the company operates across the U.S., Latin America, Atlantic, and Pacific regions through major hubs including Dallas/Fort Worth, Miami, Charlotte, and Chicago. Founded in 1926, American Airlines has built a decades-long legacy around scale, global connectivity, and aviation innovation. Its market capitalization stands at $8.56 billion.

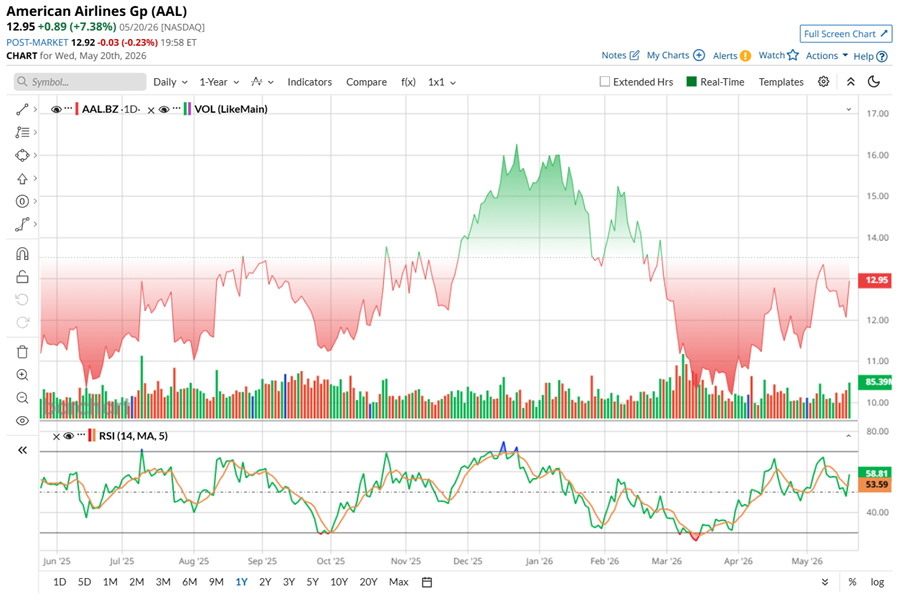

American Airlines stock has been stuck in turbulence lately. Shares of the airline giant crashed to a 52-week low of $10.09 in March before staging a 28.7% rebound, but the recovery still feels shaky. Even after the bounce, AAL remains down 15.1% in 2026 and sits well below its yearly high of $16.50. Over the past 52 weeks, the stock is up 15.79%, but investors clearly are not fully buying into the turnaround story yet.

When we look at the valuation, AAL stock trades at a discount. Its forward price-to-sales ratio of just 0.14 times sits below both its sector peers and its own five-year average. But that discount also reflects Wall Street’s hesitation, as investors remain cautious about the company’s volatile earnings outlook amid rising operating costs.

When American Airlines released its first-quarter earnings in April, the numbers showed that travelers were still spending heavily on flights despite a tougher economic backdrop. American generated a record $13.9 billion in operating revenue during the quarter, marking a 10.8% jump from last year’s quarter. Management even pointed out that the airline recorded the nine biggest revenue intake weeks in its 100-year history, highlighting solid and sustained booking demand.

The company posted an adjusted loss of -$0.40 per share, but that was still an improvement from the larger loss posted a year ago. Operationally, the quarter showed steady momentum. Total revenue per available seat mile (TRASM) rose 7.6% year-over-year (YOY) while passenger revenue per ASM (PRASM) increased 6.5%. Yield improved 5.6%, suggesting fare pricing stayed healthy across the network.

In addition, traffic trends moved in the right direction. Revenue passenger miles climbed 3.9%, while capacity expanded 3%, allowing load factor to improve 0.7 percentage points to 81.3%. Passenger revenue increased 9.7% to $12.5 billion in Q1. Cargo revenue was a brighter spot, jumping 12.9% annually to $214 million.

Meanwhile, the company was still wrestling with the cost side of the business. Total operating expenses rose 8.8% YOY to $13.95 billion, pressured by higher jet fuel prices, fuel-related taxes, and labor costs. Still, the airline made progress financially, ending the quarter with total debt down to $34.7 billion – the company’s lowest debt level since mid-2015.

Looking forward, management expects Q2 results to remain under pressure, forecasting bottom line to be anywhere between a loss of -$0.20 per share and a modest profit of $0.20 per share on an adjusted basis. Revenue growth is expected to land between 13.5% and 16.5% YOY, fueled by improving domestic performance, rising corporate travel demand, and American’s ability to gradually pass higher fuel costs through ticket pricing. For the full-year 2026, management projects the bottom line between a loss of -$0.40 per share and earnings of $1.10 per share.

However, the bigger issue is that American Airlines’ long-awaited profitability recovery hit turbulence sooner than expected. The company entered 2026 aiming to narrow the earnings gap with rivals, but the U.S.-Iran war and the resulting spike in fuel uncertainty suddenly changed the equation. Strong travel demand continues, but now investors are watching whether rising costs could once again overpower the airline’s recovery story.

Meanwhile, analysts monitoring the company expect 2026 to remain challenging, projecting a full-year loss of $0.19 per share, widening by 152.8% YOY. Still, the Street believes the pressure could ease meaningfully afterward, with losses anticipated to narrow to a profit of $2.27 per share in fiscal 2027 by 1,294.7%.

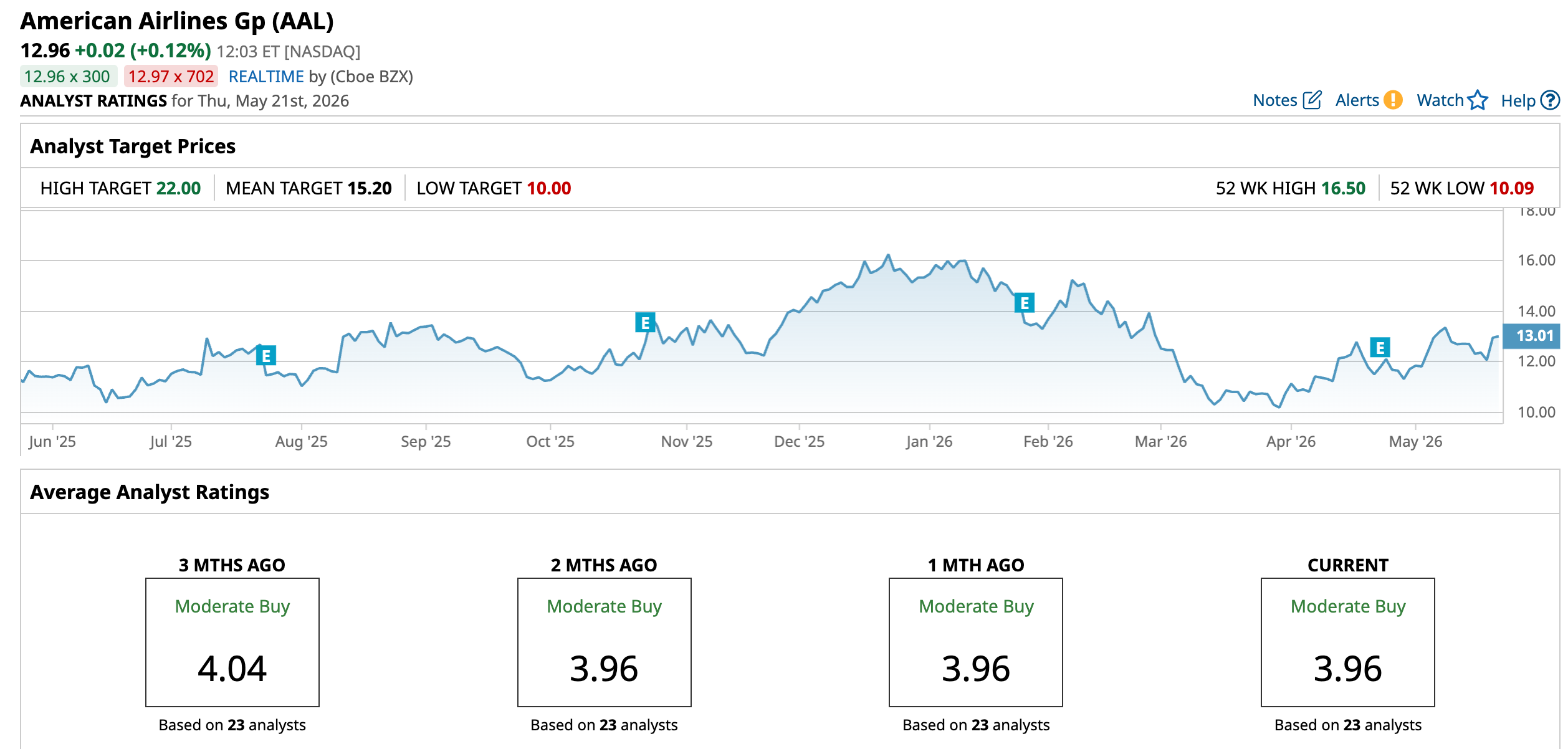

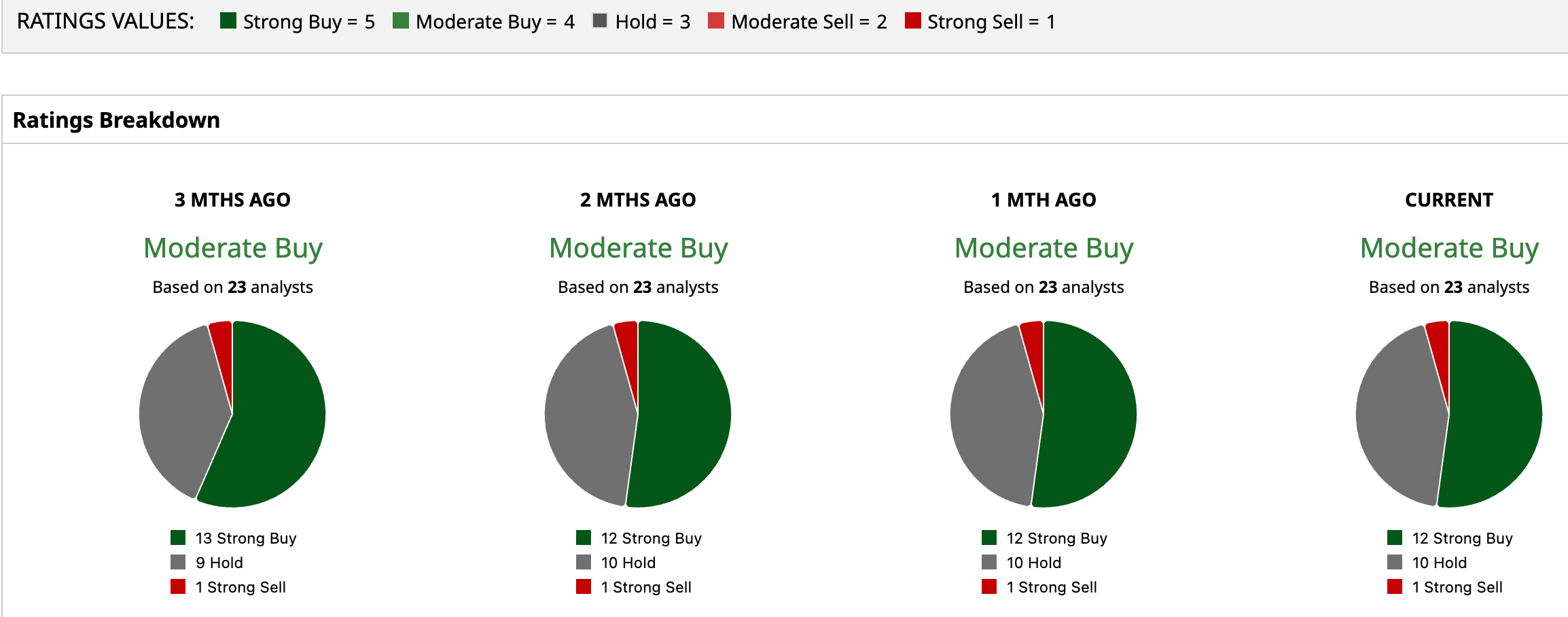

AAL has an overall consensus “Moderate Buy” rating, suggesting optimism with a dash of caution. Of the 23 analysts tracking the stock, 12 back it with a “Strong Buy,” 10 suggest a “Hold,” and the remaining one has a “Strong Sell” rating.

AAL’s average target of $15.20 suggests an upside potential of 17.3% from the current price levels. The Street’s highest $22 price target hints the stock could rally as much as 69.8%.

Airline Stock #2: United Airlines

United Airlines Holdings connects millions of travelers to more than 370 destinations across six continents each year, giving it one of the broadest international footprints in aviation. Based in Chicago, United remains a dominant player on both Atlantic and Pacific routes, linking the U.S. with major cities across Europe, Asia, Australia, Latin America, the Middle East, and Africa. With a market cap of $31.8 billion, the airline still carries global scale and reach.

But 2026 has brought turbulence. Rising jet fuel costs, fueled by geopolitical tensions, have pressured margins and prompted United to trim its full-year earnings outlook while scaling back planned flight capacity to protect profitability.

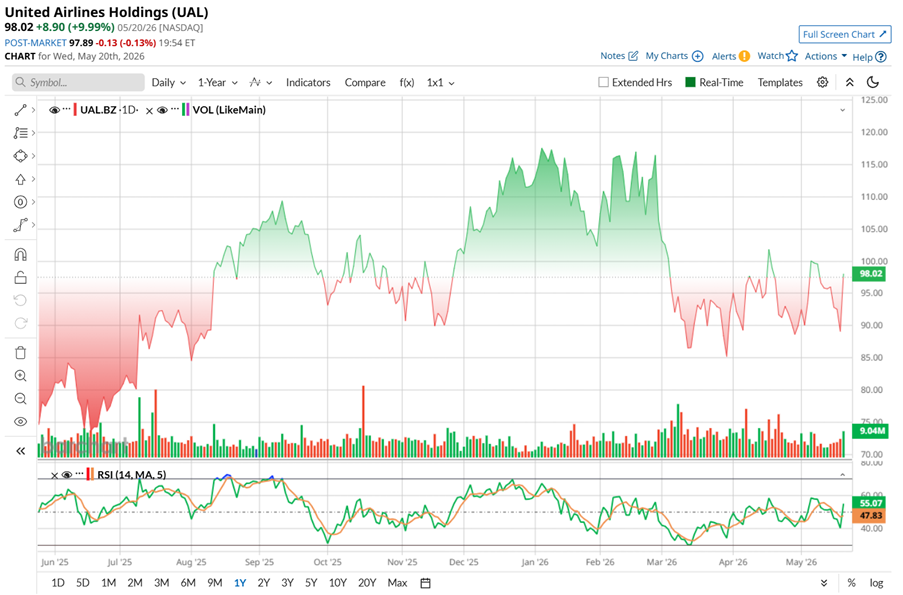

Investors have clearly noticed the shift. UAL stock is now down 13.51% in 2026 and has fallen nearly 19.4% from its January peak of $119.21. The stock still carries a solid 31.9% gain over the past year.

UAL stock may be trading at low valuation multiples for a reason. The stock’s forward price-to-earnings of 9.45 times and forward sales multiple of 0.48 times sit below airline sector averages, reflecting growing investor caution around fuel costs, softer earnings visibility, and the company’s recent decision to scale back capacity growth.

In April, United Airlines posted a record first-quarter performance, with revenue climbing 10.6% YOY to $14.6 billion and adjusted EPS jumping 30.8% annually to $1.19, both ahead of Wall Street’s expectations. Passenger revenue, which made up over 90% of total sales, rose 11% to $13.1 billion as the airline carried 42.5 million passengers, up 4.1% annually.

The quarter stood out despite a $340 million surge in fuel costs. Strong demand across premium cabins, business travel, loyalty programs, and Basic Economy helped offset the pressure. United also delivered positive PRASM growth across every region, marking its highest-revenue first quarter ever.

Traffic growth continued to outpace capacity expansion, lifting the load factor 2.4 points to 81.6%. PRASM rose 7.4%, while TRASM increased 6.9%. Yield improved 4.2% to 20.77 cents, even as fuel prices per gallon climbed nearly 10% to $2.78.

Operating expenses increased 8% YOY to $13.6 billion. United ended the quarter with $7.86 billion in cash and equivalents, alongside $21.9 billion in long-term debt and related liabilities, while also repurchasing nearly $27 million worth of shares.

Facing a sharp spike in jet fuel costs tied to the Iran conflict, the airline cut its fiscal 2026 outlook, though CEO Scott Kirby said travel demand remains resilient. But the company now expects adjusted EPS between $7 and $11 in fiscal 2026, down from its January forecast of $12 to $14 per share issued before the U.S. and Israel strikes on Iran. Adjusted capex for 2026 is projected at under $8 billion.

To offset rising costs, the carrier is trimming planned flights, a move that could tighten seat supply and support higher airfares. For Q2, United expects adjusted EPS of $1 to $2 and estimates fuel prices around $4.30 per gallon. The airline believes stronger fares and revenue will offset roughly 40% to 50% of the fuel spike in Q2, improving to as much as 80% in Q3 and potentially 85% to 100% by year-end. Capacity in the second half of 2026 is expected to range from flat to up 2%, depending on fuel conditions.

Wall Street had already been adjusting its expectations for the year because of higher fuel prices. Analysts expect United Airlines’ non-GAAP EPS to slip 11.2% YoY to $9.43 in fiscal 2026 and then rise by 45.6% annually to $13.73 in the next fiscal year.

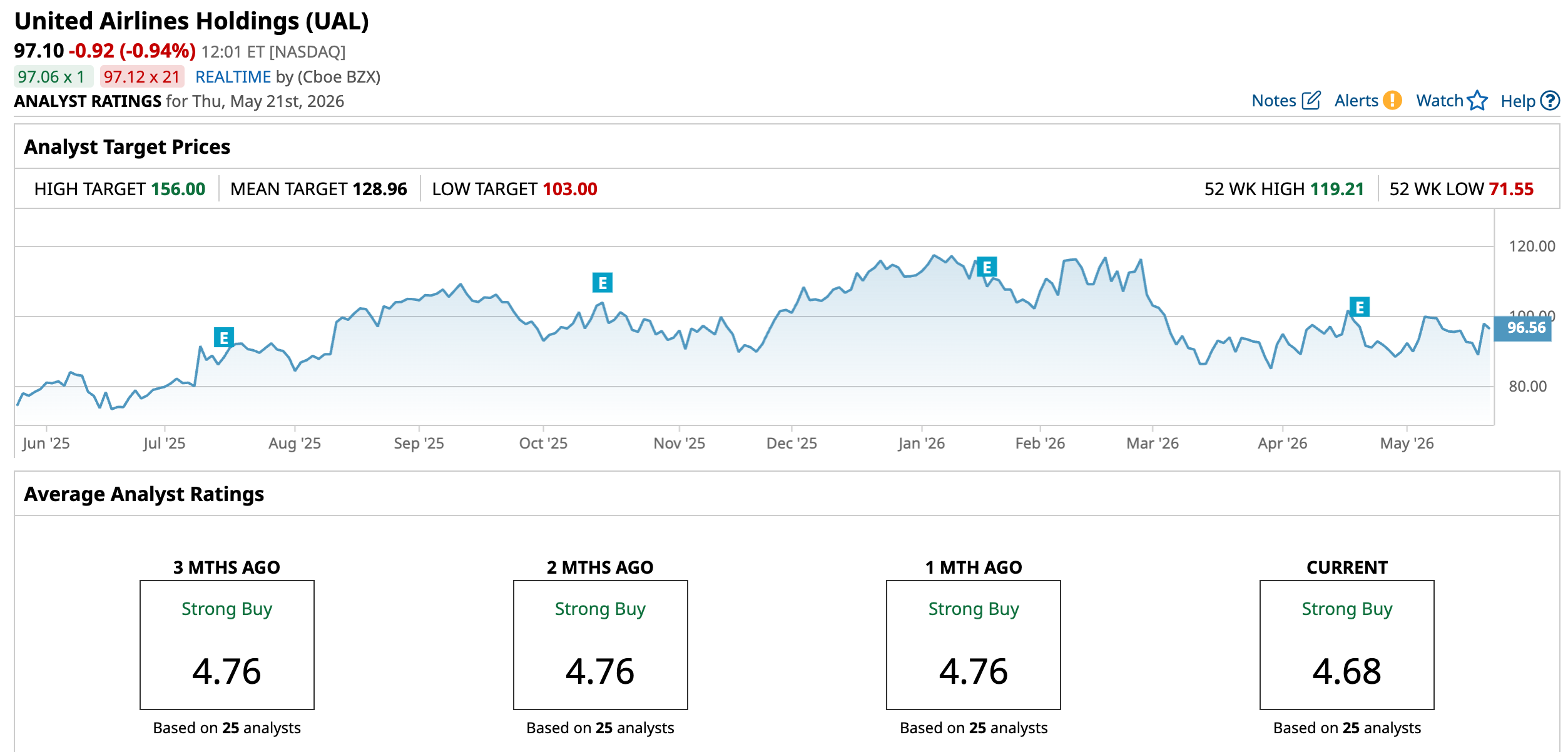

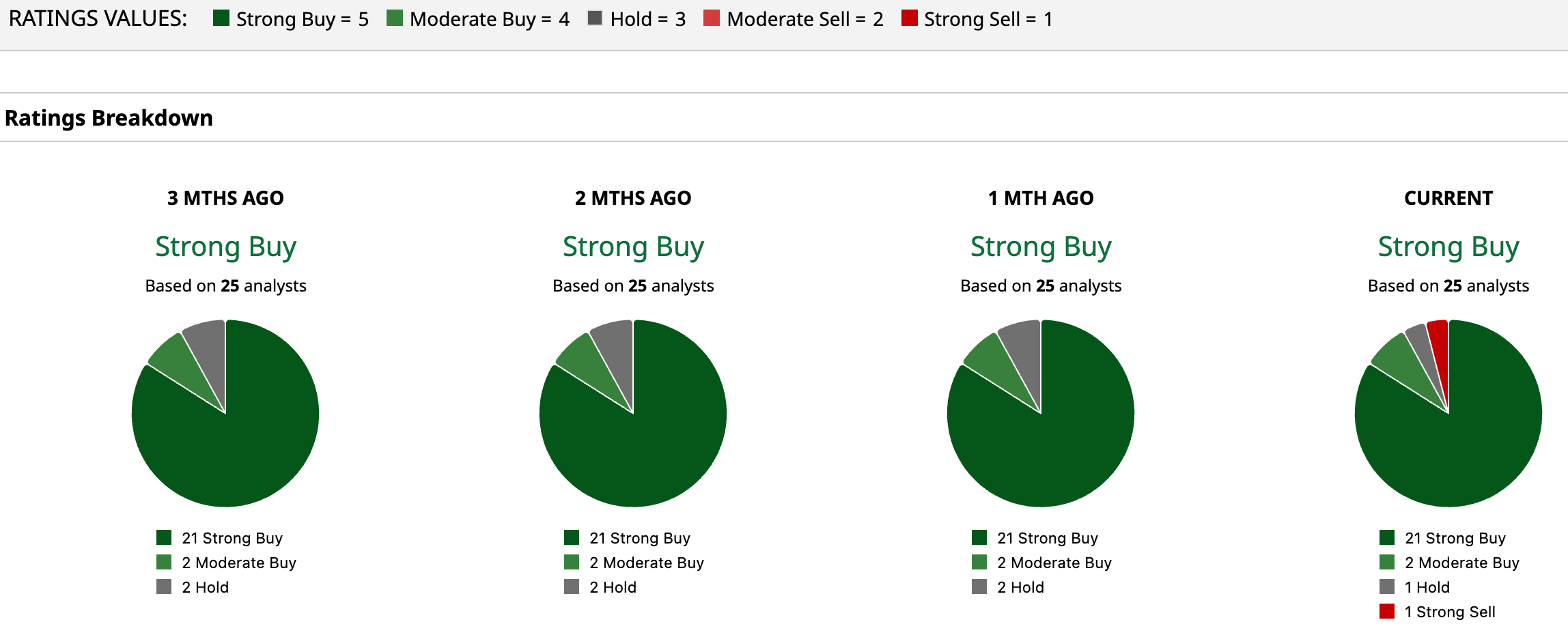

Overall, analysts are bullish about UAL’s growth prospects, giving the stock a consensus rating of “Strong Buy.” Of the 25 analysts covering the stock, 21 recommend a “Strong Buy,” while two suggest a “Moderate Buy,” one advises a “Hold,” and the remaining one has a “Strong Sell.”

The average analyst price target for UAL is $128.96, indicating potential upside of 32.8%. The Street-high target price of $156 suggests that the stock could rally as much as 60.7% from here.