/A%20close-up%20of%20the%20Lockheed%20F-104%20Starfighter%20by%20Emine%20Kamaci%20via%20Shutterstock.jpg)

eVTOL “flying car” stocks have been on edge lately, and this week Archer Aviation (ACHR) grabbed headlines by suing rival Vertical Aerospace (EVTL). Archer filed a patent infringement complaint in Texas, claiming Vertical’s new Valo air taxi unlawfully “illegally copies” design elements and flight-control tech from Archer’s in-development Midnight vehicle. Archer’s CSO laments that the Valo “suddenly mimics many of Midnight’s most distinctive design features,” calling it “a desperate attempt to copy a leader in the sector.” Vertical dismisses the allegations as “without merit” and a distraction from Archer’s own challenges.

This legal battle comes as the entire eVTOL sector shakes off 2025’s volatility. Some peers like Joby Aviation (JOBY) saw big moves, others struggled, and Archer rides waves of both bullish catalysts and skepticism. Archer briefly spiked last fall after buying Lilium patents and landing the 2028 LA Olympics air-taxi role, but it remains far from commercial revenue. Now its patent lawsuit will test investor conviction anew.

About Archer Stock

Archer Aviation is a startup to build electric vertical takeoff and landing (eVTOL) air taxis. Its flagship design is Midnight, a piloted four- or five-seat electric aircraft intended for short-range urban flights. The company has yet to generate any commercial revenue; instead, it is focused on aircraft certification, production ramps, and related tech. Archer carries a multi-billion-dollar valuation market cap of $4.5 billion despite being pre-revenue, relying on venture and public funding to bankroll development.

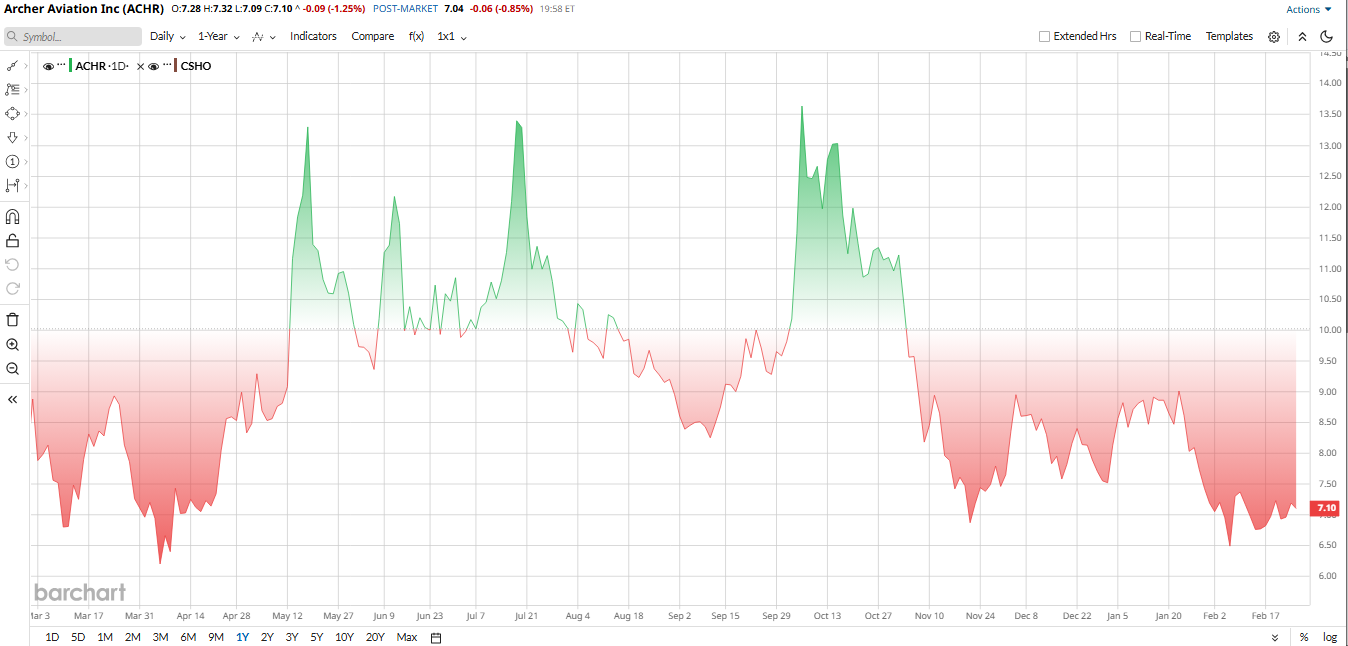

Like any other flying taxi stock, ACHR has been extremely volatile, experiencing sharp swings, as can be seen on the chart. Overall, shares are down 10% over the past 52 weeks. Analysts cited a mix of factors, including the patent purchase and major contracts, U.S. military partnerships, and the Olympics role. On the upside, versus persistent losses and cash burn on the downside. Notably, Cathie Wood’s ARK Invest scooped up shares around Q4 after an Nvidia (NVDA) partnership announcement, briefly lifting the stock. In short, Archer’s 2025 gains were largely momentum-driven, as the company still has no sales, and its year-to-date (YTD) return was modest relative to expectations, underlining how event-driven this stock can be.

However, Acher's valuation looks like a cheap bargain on the table. ACHR's price-to-book ratio is 2.04, which is 39% cheaper than the sector median of 3.36. This suggests that the stock is relatively undervalued compared to its peers.

What’s Next: Q4 2025 Earnings Preview

Archer reports its Q4 results on March 2, after the closing bell. Wall Street is modeling about a $0.25 loss per share for the quarter, an improvement from roughly $0.45 a year ago. The company has not given formal guidance, but its last capital update reiterated that spending would remain in line with prior quarters. Investors will intensely watch expenses and cash burn. Archer still has no sales, so “burn rate” is critical. So the key is keeping Q4 operating cash burn under about $110 million. Management says it has roughly $2 billion of cash on hand after recent fundraises, so as long as spending stays controlled, the company can fund itself into 2027. Broadly, the narrative will be that profitability isn’t expected yet, but narrowing losses and steady balance sheets could reassure holders.

In addition to the numbers, the earnings conference call will cover milestones. CEO Goldstein has hinted that Archer hopes to start generating revenue in Q1 2026 as flight tests advance. Analysts and traders will press on when exactly the Midnight can realistically begin service in markets like Abu Dhabi, Archer’s announced first target. Production ramp-up is also on the radar. Archer is just beginning to build out its Hawthorne, CA, plant and plans to produce sub-50 aircraft in 2026. Investors want clarity on how quickly manufacturing can scale.

Meanwhile, options traders expect volatility. The implied move after earnings is ±16%, higher than Archer’s average post-earnings swing. In short, results likely won’t change the buy/sell decision in isolation, but sharp beats or misses on expenses could swing the stock.

Recent Developments and News

Apart from the patent skirmish, Archer has had mostly positive headlines lately. It raised a hefty $302 million in February 2025 from institutional investors, including BlackRock, to extend its cash runway, and it formed Archer Defense to pursue hybrid VTOLs for the military.

Last year, Archer also signed deals with U.S. military and commercial partners, and it won the exclusive air-taxi role for the 2028 Los Angeles Olympics. In October 2025, the Lilium patent buy expanded Archer’s IP portfolio to over 1,000 patents, a move some analysts praised for strengthening its moat.

On the flip side, insiders have taken profits. Archer’s CTO sold 125,000 shares at roughly $8 in January, and Archer remains in a race where any delay is negative news. The new lawsuit against Vertical falls into a gray area: supporters say it defends innovation, and detractors worry it distracts management. At least vertically, the signal is that Archer is intent on using its patents aggressively, which could eventually deter copycat competitors.

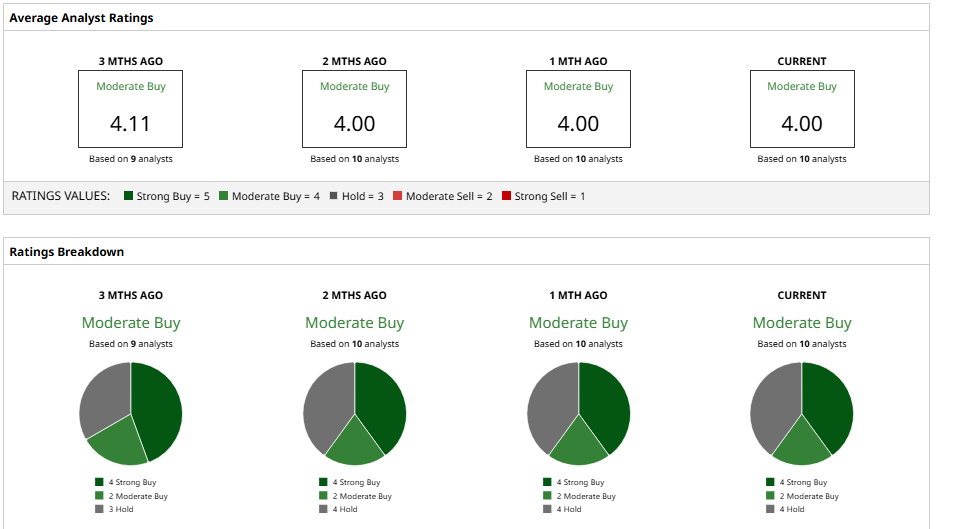

Analyst Commentary and Price Targets on ACHR Stock

Wall Street analysts are split but lean slightly positive on ACHR stock. The consensus rating is a “Moderate Buy,” with an average price target of roughly $11.60, implying potential upside of about 66% from the current stock level.

Goldman Sachs recently initiated coverage with a “Neutral” rating and an $11 target, while J.P. Morgan analyst Bill Peterson assigned a “Hold” rating with a near-term target of around $8.

In contrast, boutique brokerages are more optimistic. Canaccord Genuity gave Archer a “Buy” rating in late 2025 with a $13 price target, and Needham reiterated its “Buy” rating at $10. The most bullish outlook comes from HC Wainwright, which maintains a “Buy” rating with an $18 price target, reflecting confidence in Archer’s long-term growth potential.