With a market cap of $13.6 billion, Healthpeak Properties, Inc. (DOC) is a self-administered REIT that owns, operates, and develops high-quality healthcare real estate across the United States. The company maintains a diversified portfolio of 703 properties, focusing on outpatient medical, laboratory, and continuing care retirement community (CCRC) assets, which support healthcare discovery and delivery nationwide.

Shares of the Maryland, USA-based company have lagged behind the broader market over the past 52 weeks. DOC stock has risen 11.8% over this time frame, while the broader S&P 500 Index ($SPX) has increased 31.4%. However, shares of the company are up 21.3% on a YTD basis, outpacing SPX’s 7.6% gain.

Zooming in further, shares of the healthcare REIT have exceeded the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 7.6% return over the past 52 weeks.

Shares of Healthpeak Properties surged 18.1% following its Q1 2026 results on May 5 as the company reported adjusted FFO of $0.45 per share and revenue rose to $753 million, beating analyst expectations. Investor sentiment was further boosted after the company slightly raised its full-year 2026 adjusted FFO guidance to $1.71 per share - $1.75 per share and highlighted strong leasing activity, including 1.2 million square feet of outpatient medical and lab lease executions with positive cash releasing spreads of +5.4% for outpatient renewals and +3.5% for lab renewals.

The successful IPO of Janus Living (JAN) at the high end of its valuation range, which generated approximately $880 million in net proceeds, also strengthened investor confidence despite higher quarterly operating expenses of $747.4 million.

For the fiscal year ending in December 2026, analysts expect Healthpeak Properties’s AFFO per share to decline 5.4% year-over-year to $1.74. However, the company’s earnings surprise history is promising. It beat or met the consensus estimates in the last four quarters.

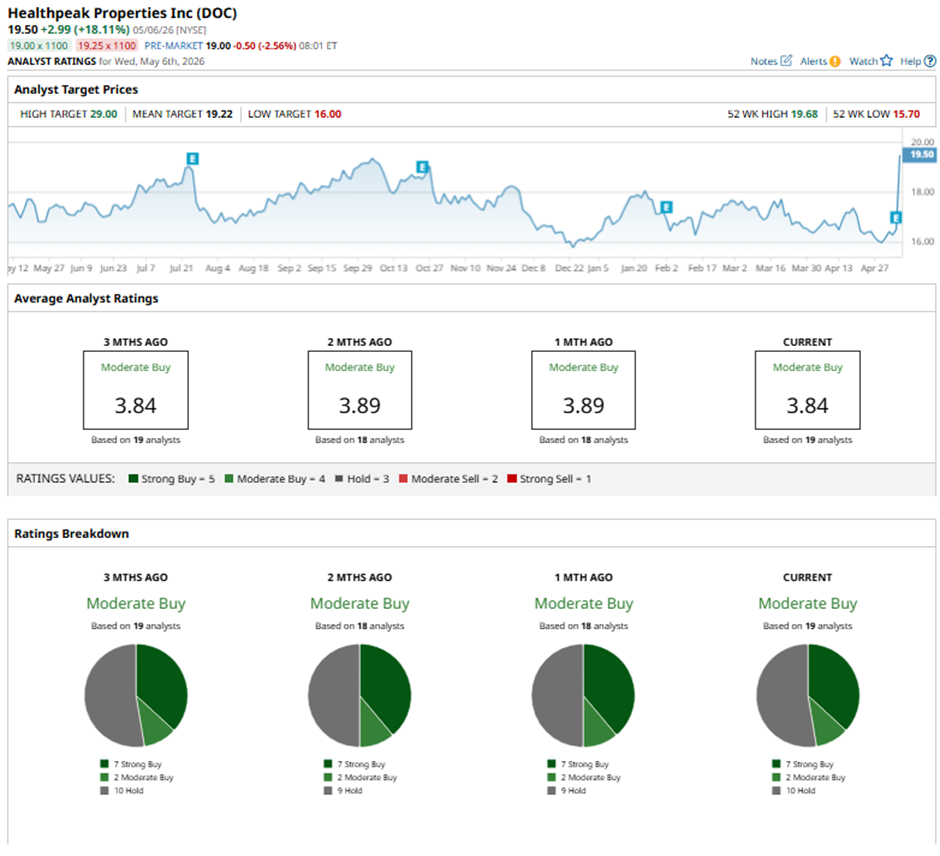

Among the 19 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings, two “Moderate Buys,” and 10 “Holds.”

On Apr. 28, Morgan Stanley cut its price target for Healthpeak Properties to $18 while maintaining an “Overweight” rating.

As of writing, the stock is trading above the mean price target of $19.22. The Street-high price target of $29 suggests a 48.7% potential upside.