/Abstract%20concept%20illustration%20of%20digital%20matrix%20by%20KanawatTH%20via%20Adobe%20Stock_.jpeg)

Training a single AI model can consume as much power as thousands of homes use in a year, and running inference on that is even more power-heavy. A small sub-$5 billion company called MDU Resources Group (MDU) is capitalizing on that and has signed an electric service agreement with Applied Digital (APLD).

Under the agreement, Montana-Dakota Utilities Company, a subsidiary of MDU, will provide Applied Digital with the infrastructure to power the Polaris Forge 3 campus. This campus is the crown jewel in Applied Digital's rapidly expanding portfolio of "AI Factories." It is a massive, purpose-built data center campus that will sell compute to CoreWeave (CRWV).

Some analysts believe this is just the first of many deals MDU Resources could sign as North Dakota sees a data center boom.

On Paper, the Deal is Solid for MDU Resources

The base lease for the Polaris Forge 3 campus is worth $7.5 billion and up to $18.2 billion if the tenant exercises all 15-year renewal options.

Polaris Forge 3 requires 430MW of electricity. That's equivalent to upwards of 400,000 average American homes that MDU Resources will have to build electrical infrastructure for. It's an arrangement that could scale rapidly if other data centers become interested, and they likely will, given how much expertise the company can amass with this huge project.

Better yet, MDU is fully insulated from electricity costs. Applied Digital itself is responsible for buying the electricity while MDU builds the infrastructure.

Why Investors Should Temper Expectations

All those big numbers aside, investors should keep in mind that Montana-Dakota Utilities is a rate-regulated utility. North Dakota caps the amount it is allowed to earn, so this deal will likely push revenue beyond the cap.

The existing Polaris Forge 1 campus near Ellendale is an example of a partnership which has credited $38.4 million back to customers in the past three years.

The newer deal is similar to that earlier deal, and the coming years may have a similar impact. MDU plans to grow its rate base, with this project not having a huge initial impact.

MDU said late last year that its $3.4 billion capex plan will lead to 7-8% annual rate base growth, with EPS growth in the similar range. Thus, this is not an explosive hypergrowth upstart that will start powering data centers en masse.

The Future of MDU Stock

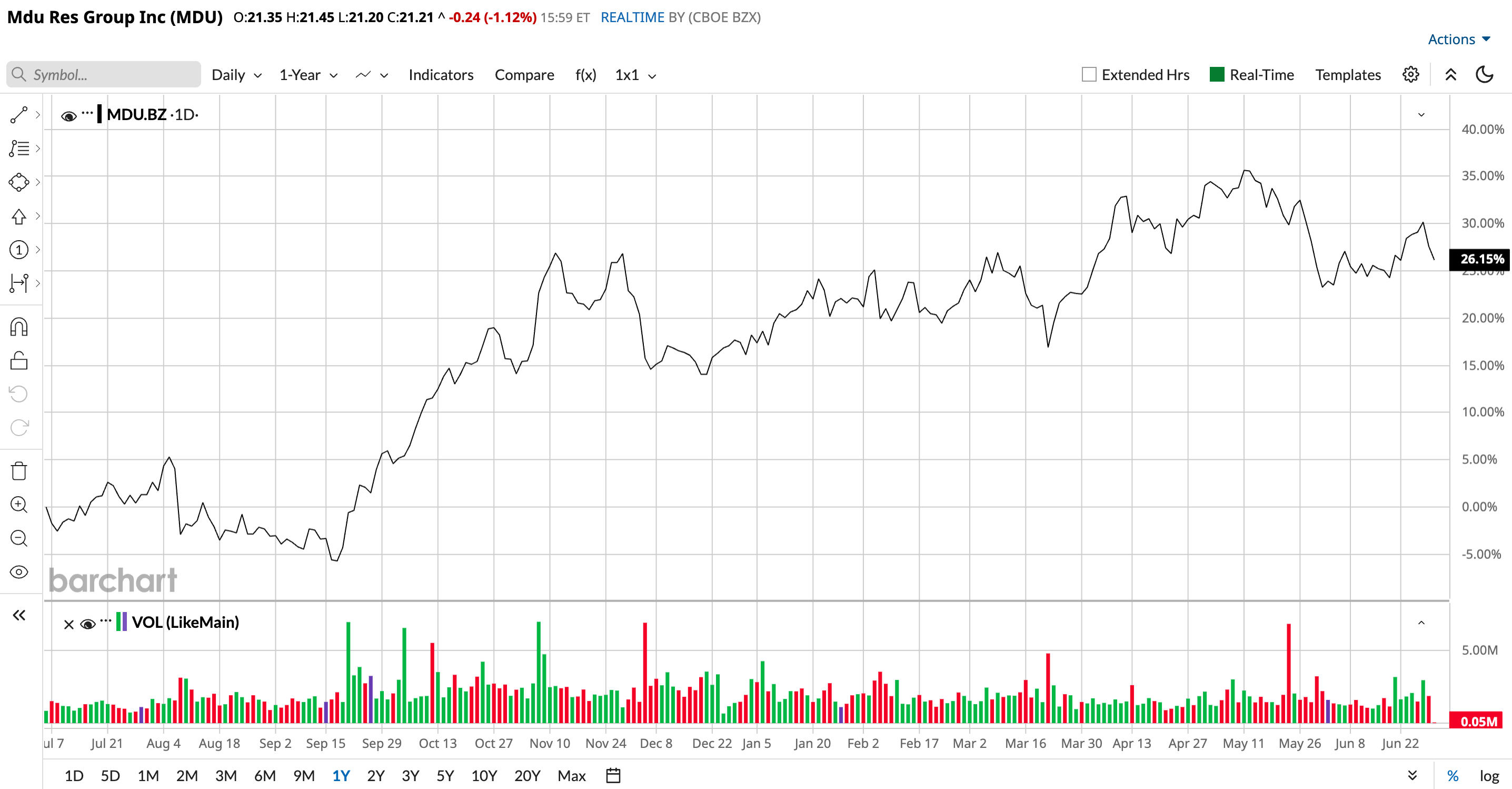

MDU is a well-established business with over 1.2 million customers already. It has remained flat like most utilities in the early 2020s but is up 27.56% in the past year. Investors are seeing this as a reliable vehicle to ride the coattails of AI without going all-in. The price-to-earnings forward Non-GAAP ratio is 21.97 times, which is higher than its historical median of 19.19 times. Investors are not paying a growth premium, though. Wall Street also likes to pay up for consistency and reliability.

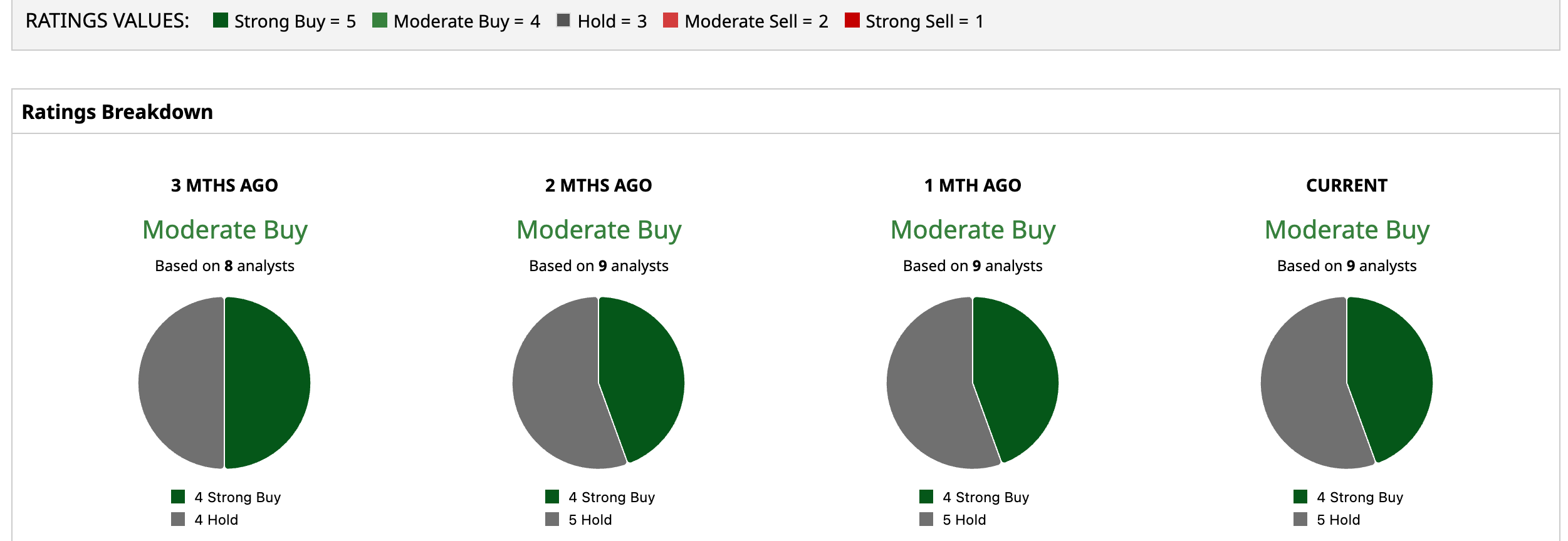

Of nine analysts rating the stock, a consensus provides a “Moderate Buy” ranking.