Last week ended on a positive note, with all the benchmark indices posting gains for the week. However, experts expect the stock market to remain volatile on concerns over surging inflation and the consequences of the Russia-Ukraine war.

The S&P 500 index is down 4.3% year-to-date. Moreover, Wall Street banks have predicted aggressive rate hikes by the Federal Reserve to bring inflation under control. And the Russia-Ukraine crisis is worsening the scenario. The CBOE Volatility Index is up 25% year-to-date.

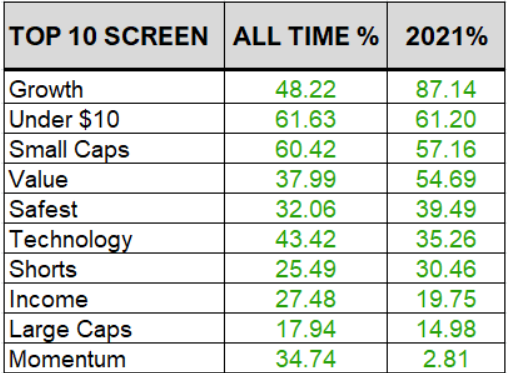

Large-cap stocks provide greater safety and value than small to mid-cap stocks because of their market dominance and higher financial flexibility. That’s why today we're highlighting 3 exciting stocks from our Top 10 Large-Cap screen, which is just 1 of the 10 screens in our POWR Screens 10 service (more on that below). Bristol-Myers Squibb Company (BMY), Vertex Pharmaceuticals Incorporated (VRTX), and Molina Healthcare, Inc. (MOH) have outpaced the S&P 500 so far this year and could be great additions to your portfolio.

Bristol-Myers Squibb Company (BMY)

BMY is a developer, licenser, manufacturer, and marketer of biopharmaceutical products worldwide. The company’s offerings include Revlimid, an oral immunomodulatory drug for treating multiple myeloma. It has a market capitalization of $159.73 billion.

On March 18, BMY announced that the United States Food and Drug Administration (FDA) had approved OpdualagTM (nivolumab and relatlimab-rmbw), administered as a single intravenous infusion for the treatment of adult and pediatric patients 12 years or older with unresectable or metastatic melanoma. This might add to the company’s revenue stream.

On March 1, BMY declared a quarterly dividend of $0.54 per share on the company’s $.10 par value common stock, payable to shareholders on May 2. Additionally, the company announced a quarterly dividend of $0.50 per share on its $2.00 convertible preferred stock, payable on June 1. This reflects upon the company’s ability to pay back shareholders.

For the fiscal fourth quarter ended December 31, BMY’s total revenues increased 8.3% year-over-year to $11.99 billion. Non-GAAP net earnings attributable to BMY rose 22.2% from the prior-year quarter to $4.07 billion, while non-GAAP EPS improved 25.3% from the same period the prior year to $1.83.

Analysts expect BMY’s EPS to increase 11.5% year-over-year to $1.94 in the fiscal quarter ending March 2022. Likewise, Street expects revenue for the same period to rise 3.2% from the prior-year quarter to $11.42 billion. In addition, BMY has topped consensus EPS estimates in three out of the trailing four quarters, which is impressive.

The stock has gained 17.5% year-to-date and 6.5% over the past month to close Friday’s trading session at $73.28.

BMY’s strong fundamentals are reflected in its POWR Ratings. The stock has an overall rating of A, which equates to a Strong Buy in our proprietary rating system. The POWR Ratings are calculated by considering 118 different factors, with each factor weighted to an optimal degree.

BMY has a Value grade of A and a Growth and Quality grade of B. In the 175-stock Medical – Pharmaceuticals industry, it is ranked #2.

To see the additional POWR Ratings for Momentum, Stability, and Sentiment, click here.

Vertex Pharmaceuticals Incorporated (VRTX)

VRTX develops and commercializes therapies for treating cystic fibrosis, a condition that causes persistent lung infections. The company’s offerings include SYMDEKO/SYMKEVI, ORKAMBI, and KALYDECO therapies for treating patients with the disease. It has a $64.65 billion market capitalization.

On March 25, VRTX announced that Health Canada had granted Marketing Authorization for the expanded use of PrKALYDECO® (ivacaftor) for treating patients from 4 months to 18 years of age living with the R117H mutation in the cystic fibrosis transmembrane conductance regulator (CFTR) gene. On January 11, VRTX announced that the European Commission had approved the label extension of KAFTRIO in a combination regimen with ivacaftor for patients between the ages of six and 11. These approvals might prove to be profitable for VRTX.

VRTX’s non-GAAP total revenues increased 27.4% year-over-year to $2.07 billion in the fiscal fourth quarter ended December 31. Non-GAAP net income and non-GAAP net income per common share came in at $865.90 million and $3.37, respectively, up 31.1% and 34.3% from the prior-year quarter. Non-GAAP operating income rose 26.7% from the same period the prior year to $1.12 billion.

Analysts expect VRTX’s EPS to increase 16.8% year-over-year to $3.48 for the quarter ending March 2022. Likewise, Street expects revenue to improve 25.4% from the prior-year quarter to $2.08 billion for the same quarter. In addition, VRTX has an impressive surprise earnings history, as it has topped consensus EPS estimates in each of the trailing four quarters.

VRTX’s shares have gained 10.3% over the past month to close Friday’s trading session at $253.95. It has gained 15.6% year-to-date.

It’s no surprise that VRTX has an overall A rating, which translates to Strong Buy in our POWR Rating system.

VRTX has an A grade for Quality and a B grade for Growth, Value, and Sentiment. In the 422-stock Biotech industry, it is ranked #1.

To see the additional POWR Ratings for Momentum and Stability for VRTX, click here.

Molina Healthcare, Inc. (MOH)

MOH is a managed healthcare services provider to low-income families and individuals under the Medicaid and Medicare programs and through state insurance marketplaces. The company operates through the four broad segments of Medicaid; Medicare; Marketplace; and Other. It has a market capitalization of $19.96 billion.

On January 3, MOH announced the closing of its acquisition of Cigna Corp’s (CI) Texas Medicaid contracts. This might prove to be beneficial for the company.

For the fiscal fourth quarter ended December 31, MOH’s total revenue increased 41.5% year-over-year to $7.41 billion. Adjusted net income and adjusted EPS came in at $170 million and $2.88, up substantially from their negative year-ago values, respectively.

The consensus EPS estimate of $4.66 for the quarter ending March 2022 indicates a 5% year-over-year increase. Likewise, the consensus revenue estimate for the same quarter of $7.53 billion reflects an improvement of 15.4% from the prior-year quarter. Additionally, MOH has beaten consensus EPS estimates in each of the trailing four quarters.

The stock has gained 45.2% over the past year and 6.9% year-to-date to close Friday’s trading session at $340.11.

This promising outlook is reflected in MOH’s POWR Ratings. The stock has an overall A rating, equating to Strong Buy in our proprietary rating system.

MOH has a Growth, Value, and Quality grade of B. It is ranked #3 out of 11 stocks in the Medical – Health Insurance industry. The industry is rated B.

In addition to the POWR Rating grades we’ve stated above, one can see MOH ratings for Momentum, Stability, and Sentiment here.

Want more stocks like these?

These three stocks are just a fraction of what you will find in our coveted Top 10 Large- Cap strategy. And the value strategy is just a fraction of what you get with our popular service; POWR Screens 10.

POWR Screens provides 10 market beating strategies with exactly 10 stocks each. Truly something for every investor with verified performance.

Learn More About POWR Screens 10 >>

BMY shares were trading at $72.89 per share on Monday afternoon, down $0.39 (-0.53%). Year-to-date, BMY has gained 17.93%, versus a -4.01% rise in the benchmark S&P 500 index during the same period.

About the Author: Anushka Dutta

Anushka is an analyst whose interest in understanding the impact of broader economic changes on financial markets motivated her to pursue a career in investment research.

3 Red-Hot Large-Cap Stocks Outpacing the S&P 500 StockNews.com