P/E, the price-to-earnings multiple, is a measure of stock value relative to earnings power and a cornerstone of value investing. Stocks with lower price multiples are cheaper to own relative to their earnings power, indicate value for investors, and have the potential for significant price gains over time.

Additionally, low P/E stocks typically have their bad news priced in, offer limited downside relative to higher-valued stocks, provide higher-than-average yields, and offer the opportunity for multi-bagger gains. The combination of improving fundamentals and earnings growth provides a dual-market-tailwind and leverage for price action as stocks are revalued and premiums are priced in. The risk is that low P/E stocks are cheap for a reason. In this scenario, there is little hope for stock price gains. This is a look at five low P/E stocks and whether they present opportunities for gains in 2026.

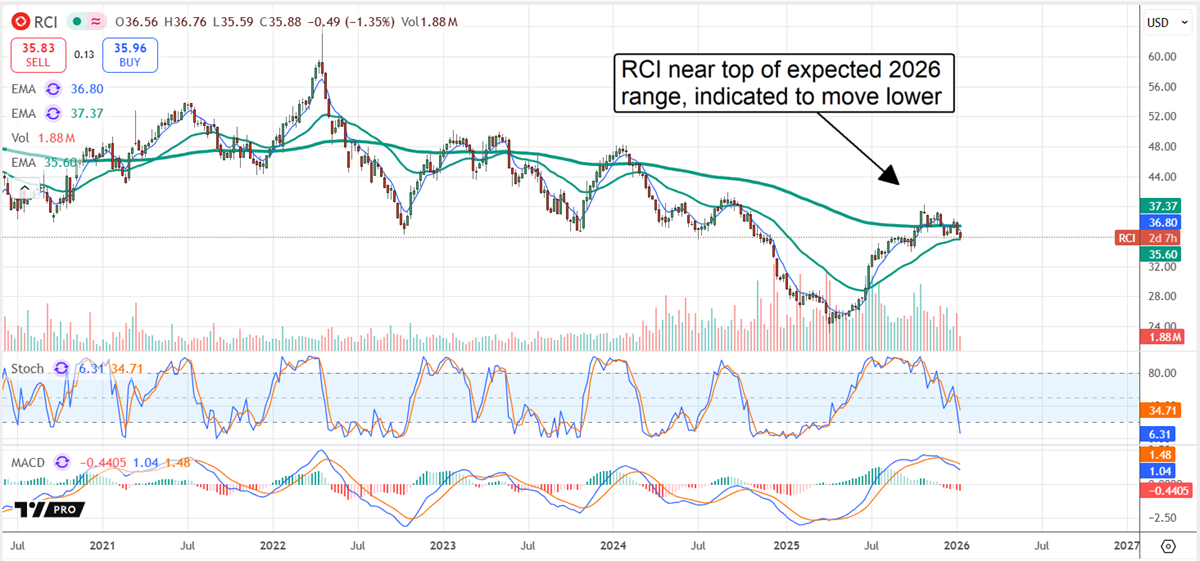

Why Rogers’ High Yield Comes With Limited Upside

Rogers Communications (NYSE: RCI) is a Canadian communications and media company. It trades at a low 10x current-year earnings, suggesting it could rise by 100% to align with broad market averages. The problem is that this company, whose dividend yields more than 4% as of early 2026, trades in alignment with media peers and has a tepid outlook for the year. Not only is earnings growth questionable, but so too is dividend growth. The company’s payment history is spotty, with irregular quarterly distributions and recent declines.

Likewise, analysts and institutional trends provide no reason to expect this stock price to rise in 2026. Analysts rate it a Hold but have significantly reduced their price targets over the trailing twelve months, resulting in a price point below consensus. Consensus assumes fair value in mid-January, suggesting a likely downside move. Meanwhile, institutions provide mediocre support, owning about 45% of the stock and distributing shares at the start of the year.

Comcast Combines High Yield With Rebound Potential in 2026

Comcast Corporation (NASDAQ: CMCSA) is another communications and media company trading at a low P/E multiple. The difference is that this stock trades at only 7x its current-year earnings, indicating a value relative to its peers, along with a 4.5% dividend yield. This company will report a decline in revenue and earnings due to divestiture, but its core results are expected to grow, and expectations are modest. This sets the company up to outperform and drive a bullish analyst revision cycle, and the analysts are already optimistic on the stock price.

An analyst reset helped depress CMCSA stock prices in 2025, but two factors set the market up to rebound in 2026. The first is that the CMCSA market oversold, and the most recent targets align with the consensus forecast for a 20% stock price increase. Institutional activity also aligns with a rebound in early January, as they own more than 65% of the stock and bought at a pace of $3 for each $1 sold the first two weeks of the year.

HP Inc. Looks Positioned for a Powerful Rebound in 2026

HP Inc.’s (NYSE: HPQ) share price is affected by AI, as DRAM shortages are curtailing supply and limiting production. The impact caused analysts to reset their price targets. However, as with Comcast, this market has oversold and is setting up for a rebound. While the outlook is depressed, this company is expected to sustain modest growth over the next few years and generate sufficient earnings to support its capital return. The capital return includes a dividend yielding more than 5.5% annualized as of early January, along with an expectation of distribution growth. HP Inc. pays less than 40% of its earnings, has increased its dividend for 15 consecutive years, and has a 10% CAGR.

Analysts are optimistic. Their reset reduced consensus in 2025, but late-year and early-2026 updates have reaffirmed it. The takeaway is that this stock is expected to rise by at least 20%, and the 20% stock price gain indicated is the trigger for another 20% to 30% gain when achieved. Looking at the chart, HPQ stock is at its long-term lows, and the MACD is diverging from the price movement. The divergence is a critical indicator, as it signals a weakening downtrend with bulls ready to regain control.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "3 Low P/E Stocks: Separating Multibaggers From a Value Trap" first appeared on MarketBeat.