Prospective homeowners are facing a significantly reduced choice of mortgage products, with nearly a fifth of available deals vanishing in just two weeks, according to new analysis.

Financial information website Moneyfacts reported that as of Monday morning, 1,492 fewer residential mortgage products were on offer compared to 9 March, marking a 19.5 per cent contraction in the market.

A substantial 744 deals disappeared in the period since last Thursday alone.

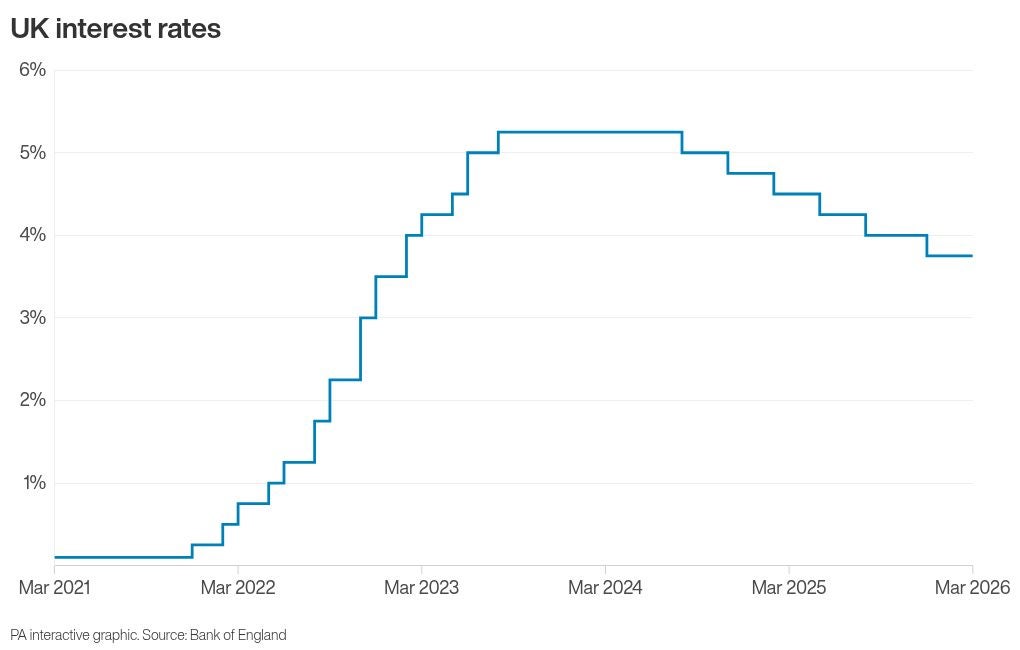

This rapid decline follows last Thursday's decision by the Bank of England to maintain its base rate at 3.75 per cent, a day which also saw increased forecasts for UK inflation.

Lenders have been scrambling to increase the mortgage rates they are offering and withdraw some products amid changing expectations for inflation, with the conflict in the Middle East putting pressure on prices.

Swap rates, which are used by lenders to price mortgages, have been rising in recent weeks.

Expectations that the Bank of England is set to cut the base rate this year have also gone into reverse, with some finance experts suggesting increases could be made amid the sharper rises in inflation than were previously expected.

The Bank of England’s Monetary Policy Committee now expects Consumer Prices Index (CPI) inflation to be around 3 per cent in the second quarter of 2026, up from the 2.1 per cent that had been forecast in February, with a potential rise in inflation up to 3.5 per cent in the third quarter.

Moneyfacts said homeowners will find the the average two-year fixed-rate mortgage has risen from 4.83 per cent at the start of March to 5.43 per cent on Monday morning.

The average five-year fixed-rate deal on the market has risen from 4.95 per cent at the start of March to 5.45 per cent.

Adam French, head of consumer finance at Moneyfacts, said: “Rates continue to climb as lenders scramble to keep pace with rising funding costs.

“The average two-year fixed-rate has gone from 4.83 per cent at the start of March to 5.43 per cent today, its highest level since February 2025. The average five-year fix has gone from 4.95 per cent to 5.45 per cent, now at its highest since July 2024. Even the very cheapest deals have shifted significantly.”

He said: “The combination of rising rates and falling choice is a direct response to the conflict in the Middle East which has dramatically shifted expectations around inflation and interest rates. Many deals are likely to return to the market in the coming days and weeks but repriced at higher rates.

“While a quicker resolution to the conflict could ease some of the pressure on rates, the reality is that a more volatile world is a more expensive world.

“Even though the most competitive deals will remain below average, anyone looking to buy or remortgage this year needs to prepare for higher costs than previously expected.”

Despite the shrinking choice of mortgage deals for homeowners in recent weeks, the fall has not been as sharp as in the aftermath of the mini-budget in 2022.

The biggest single-day fall for residential mortgages recorded by Moneyfacts was the withdrawal of 935 products on September 27 2022, which it has said was a little over 25 per cent of the deals available at the time.

Nicholas Mendes, mortgage technical manager at John Charcol, said: “There are understandable comparisons with the volatility seen after the Liz Truss mini-budget, because the pattern of rapid withdrawals and repricing feels familiar.

“But the cause is different. In 2022, the shock was driven by domestic fiscal credibility.

“This time, the pressure is coming from a sharp shift in rate expectations, higher swap pricing, and concern that policy may need to stay tighter for longer.

“That does not automatically mean a return to those peak mortgage rates, but it does raise the risk of further upward moves in the near-term.”

He said that speaking to a broker early could potentially help borrowers, adding that for those coming up to a remortgage: “In most cases, a new rate can be secured three to six months before an existing deal ends.

“If rates improve before completion, there is often scope to switch to something lower, meaning you save a significant amount over the term of the mortgage.”

Aspiring first-time buyers with student debt ‘face £2,000 annual savings gap’

Many households ‘will only have cleared their Christmas debt in the weeks ahead’

Bank of England unanimously votes to pause interest rates as Iran worries grow

Regulator to review later life mortgages as Britons face retirement shortfall

The most and least affordable locations for first-time buyers in UK

Major UK stockbroker outage leaves customers unable to check accounts